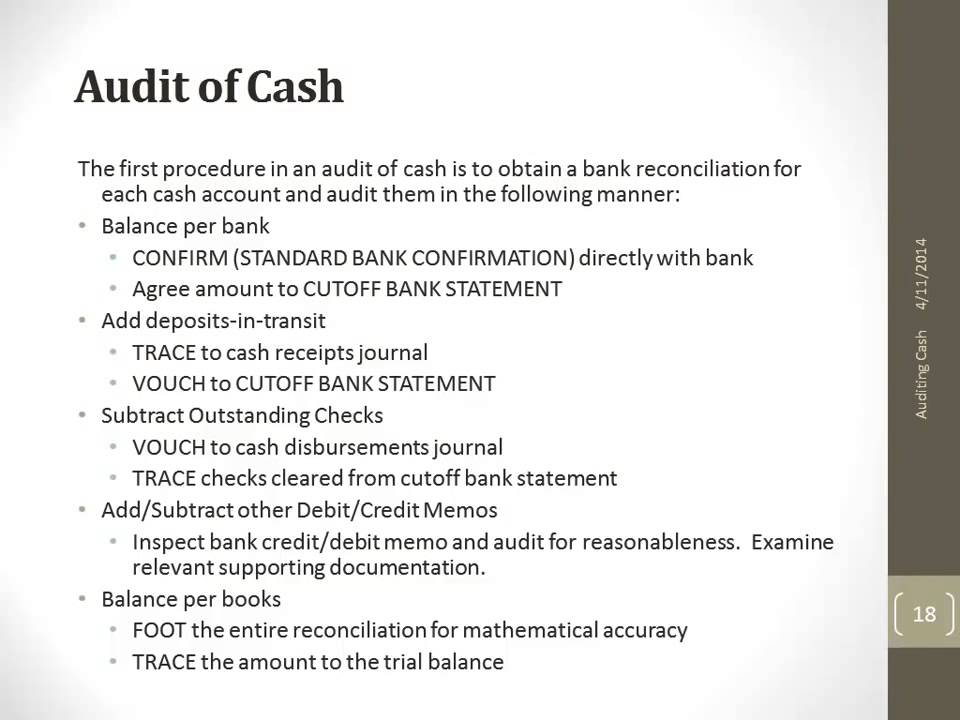

Effective Audit Procedures for Cash Transactions

Understanding the role of walkthroughs in internal audits

Key Insights

- Walkthroughs Offer a Complete Picture: They trace the cash transaction from origination to recording.

- Identification of Weaknesses: Walkthroughs expose gaps or inefficiencies in the control environment.

- Interactive and Comprehensive: Combining observation with inquiry provides robust evidence of control effectiveness.

Overview of Audit Procedures in Cash Transactions

In the context of internal audits for cash transactions, multiple procedures are available for auditors to assess the reliability of the control environment. These procedures include assessing IT system controls, conducting staff interviews, reviewing bank statements, and performing walkthroughs of cash handling procedures. After careful synthesis of key points from various expert sources, it is evident that walkthroughs of cash handling procedures are widely recognized as the most effective audit tool for evaluating the control environment.

Common Audit Procedures

Assessing IT System Controls

Assessing IT system controls involves examining the automated components of a company’s control environment. This method includes reviewing system configurations, access controls, and automated reconciliations, ensuring that digital systems support transaction security and integrity. Although crucial for identifying potential data manipulation or unauthorized access, these assessments can be limited because they primarily focus on the integrity of system processes rather than the actual implementation of operational procedures on the ground.

Conducting Staff Interviews

Interviews with staff provide valuable qualitative insights. Through these interactions, auditors gain an understanding of employee knowledge and the practical application of cash handling policies and procedures. However, while interviews can reveal general adherence to policy and potential areas of concern, they are inherently subjective. Responses may sometimes be overly optimistic or not reveal actual gaps in operational procedures. Therefore, interviews tend to complement other audit techniques rather than serve as a standalone method.

Reviewing Bank Statements

The examination of bank statements is a critical quantitative procedure that allows auditors to verify cash inflows and outflows. This method ensures that recorded transactions match what is evidenced by external financial institutions. It is particularly useful for identifying discrepancies and ensuring transactions have been accurately reviewed. However, bank statement reviews offer a retrospective look, which may not capture real-time operational weaknesses or subtle misapplications of designed controls.

Walkthroughs of Cash Handling Procedures

Walkthroughs distinguish themselves as the most comprehensive method for assessing the internal control environment. A walkthrough involves following a cash transaction throughout its entire lifecycle—from the point of its initiation to its ultimate reflection in the financial records. This method requires the auditor to observe the same processes and utilize the same documentation as the staff, fulfilling several critical functions:

- Detailed Process Understanding: By tracing each transaction, auditors gain a deep understanding of the operational workflow, including how transactions are initiated, processed, and recorded.

- Identification of Control Weaknesses: Walkthroughs help pinpoint areas where the control environment may be deficient, such as insufficient segregation of duties or lapses in the verification process.

- Interactive Verification: During walkthroughs, auditors can engage with operational staff by asking detailed questions. This interactive approach provides clarity on whether the documented procedures align with actual practices.

- Risk Assessment: Following transactions ensures that auditors are not solely relying on recorded data but are actively identifying potential risks related to misstatements or procedural inadequacies.

Deep Dive into Walkthroughs

Understanding the Walkthrough Process

The walkthrough procedure is a thorough evaluation that goes beyond mere observation. It is designed to test the design and operational effectiveness of the cash handling controls. Typically, this process begins by selecting a representative sample of cash transactions. The auditor then follows these transactions through every step in the control process, using the same documents and systems employed by the staff. Here are the steps commonly observed during a walkthrough:

Initiation of the Transaction

The process begins with locating and understanding where and how a cash transaction is initiated. This includes reviewing documents such as receipts, cash registers, or electronic point-of-sale systems. At this stage, the auditor verifies that the transaction inception adheres to the predefined control protocols.

Processing and Handling

Once initiated, the transaction must be processed appropriately. This includes reviewing the internal controls related to cash counts, validation of amounts, and ensuring that there are checks such as dual custody or segregation of duties. Walkthroughs during processing are crucial as errors or malpractices often occur at this juncture.

Recording in Financial Systems

After processing, the final stage involves ensuring that the transaction is accurately recorded in the financial system. This step confirms that the initial cash receipt or disbursement is reconciled in the system, providing assurance that external bank statements and internal records are consistent.

Advantages of Walkthroughs

Compared to other audit procedures, walkthroughs offer several distinct benefits:

| Aspect | Walkthrough Benefits | Alternative Procedures |

|---|---|---|

| Comprehensiveness | Provides end-to-end insight into the entire transaction lifecycle and uncovering process inefficiencies. | IT control reviews and bank statement analyses provide partial or retrospective views. |

| Real-time Verification | Enables observation of operational practices as they occur, revealing discrepancies between documented policy and practice. | Interviews provide subjective assessments but may lack evidentiary support. |

| Risk Identification | Direct observation helps in identifying unforeseen risks like human error or process bottlenecks. | Banking reviews demonstrate final recorded data without showing the process errors. |

| Staff Engagement | Encourages detailed discussions with personnel to clarify operational issues and misconceptions. | Interviews face limitations in verifying actual behavior versus reported practices. |

The table above encapsulates the comparative strengths of walkthroughs against other common audit methods, such as assessing IT controls, conducting staff interviews, and reviewing bank statements.

Implementing Walkthroughs: A Practical Guide

Planning and Execution

To successfully implement walkthroughs in an internal audit of cash transactions, auditors need a structured plan that includes:

Identifying Key Transactions

It is critical to start by identifying a set of representative transactions that capture the range of activities within the cash handling process. This selection should reflect variations in transaction size, frequency, and the departments involved.

Document Collection and Process Mapping

Once the transactions are identified, collect all relevant documentation such as receipts, register copies, authorization forms, and reconciliation reports. Creating a process map that visually delineates each step in the cash handling procedure can be an effective tool for planning the walkthrough.

Observation and Inquiry

During the walkthrough, the auditor follows the cash flow through the process. This involves:

- Observing and confirming that all control measures (e.g., segregation of duties, proper authorizations) are in place.

- Interviewing staff about how they perform their tasks and assessing whether the documentation aligns with the described processes.

- Comparing the observed activities with the formal policies and procedures to identify any deviations.

Documenting Observations

Meticulous documentation is essential during walkthroughs. Auditors should record details of the entire process, noting any discrepancies, delays, or instances of non-compliance. This reporting not only forms the basis of the subsequent evaluation but also helps in communicating internal control weaknesses to management.

Evaluating the Control Environment

A key benefit of using walkthroughs is the ability to evaluate both the design and the operational effectiveness of the controls. By following transactions in real-time, auditors are better equipped to understand the interplay between different components of the control environment. They can assess:

- Whether established procedures are being followed systematically.

- If redundancies exist that might prevent or detect errors or fraud.

- The overall responsiveness of the process when anomalies or discrepancies are observed.

Continuous evaluation during a walkthrough allows auditors to provide immediate feedback, which can be instrumental in mitigating risks early on. For instance, if an auditor notes insufficient segregation of duties during the cash handling process, this observation can lead to corrective actions before further discrepancies occur.

Integrating Multiple Audit Methods

While walkthroughs of cash handling procedures are highly effective, it is important to recognize that they function best as a part of a comprehensive audit strategy. Other procedures such as IT system reviews, staff interviews, and bank statement analyses have their place in forming a complete picture of the control environment:

Complementary Roles

Each audit method contributes unique insights:

- Assessing IT System Controls: Confirms that automated systems supporting cash handling are secure and operating effectively. Although IT controls can highlight discrepancies in data integrity, they are generally more technical and require integration with operational insights.

- Conducting Staff Interviews: Provides clarity on the human element behind the controls. Interviews can unearth informal practices or workarounds that might not be apparent in documented procedures.

- Reviewing Bank Statements: Offers a reconciled view of recorded transactions against external financial data, thus ensuring that the recorded figures match the actual cash flows.

When combined, these methods offer a balanced audit approach—walkthroughs create a solid foundation by directly observing the process, while other methods can verify and supplement the findings, ensuring a robust understanding of the entire control framework.

Risk Management and Internal Controls

Enhancing the Reliability of Cash Transactions

The core aim of any internal audit is to ensure that the control environment is both reliable and effective in mitigating risks. Walkthroughs inherently contribute to this by:

- Detecting discrepancies or breakdowns in the system before they result in significant misstatements.

- Providing evidence of adherence to internal control policies, which is essential for accurate financial reporting.

- Allowing auditors to evaluate how well the current processes are equipped to prevent fraud and error.

Real-world Application

In real-world scenarios, organizations often operate under tight control structures where errors in cash handling can lead to significant financial discrepancies. By performing walkthroughs, auditors assess how such errors are prevented, detected, or corrected in real-time. If a walkthrough reveals a procedural lapse—such as inadequate reconciliation of cash receipts—it serves as a strong prompt for management to review and improve their control systems. This proactive approach not only aids in regulatory compliance but also enhances the overall governance of the organization.

Supporting Evidence and Key References

The consensus among specialists, auditing standards, and practical examples emphasizes that walkthroughs of cash handling procedures are the preferred method in internal audits. Leading resources such as the PCAOB standard AS 2201 and insights from various internal auditing experts underline the effectiveness of walkthroughs in explaining the design and operation of controls as well as identifying potential weaknesses.

| Resource | Focus Area |

|---|---|

| PCAOB AS 2201 | Standards for walkthroughs and audit procedures |

| Hyperproof | Audit procedures and internal controls |

| ZenGRC | Detailed insights into internal controls for cash transactions |

| CPA Hall Talk | Best practices in auditing cash |

| Diligent | Procedures and guidelines on internal controls for cash |

Through extensive review and integration of audit methodologies, it becomes clear that while every audit procedure has a role, walkthroughs are uniquely positioned to comprehensively assess the control environment, making them the most effective audit procedure in this context.

References

- PCAOB AS 2201 - PCAOB

- Audit Procedures and Internal Controls - Hyperproof

- Internal Controls for Cash - Diligent

- Internal Controls for Cash - ZenGRC

- Auditing Cash Transactions - CPA Hall Talk

Recommended Related Queries

Last updated March 7, 2025