Mastering Crypto Portfolio Optimization: Reinforcement Learning Meets Learning to Rank

A data-driven methodology for maximizing returns while minimizing risk in cryptocurrency trading using AI

Essential Highlights

- Reinforcement learning combined with Learning to Rank (LTR) creates a powerful framework for dynamic cryptocurrency portfolio optimization that adapts to changing market conditions.

- Comprehensive feature engineering covering technical indicators, market sentiment, and on-chain metrics provides the AI model with a holistic view of cryptocurrency performance potential.

- Continuous backtesting, retraining, and model monitoring are crucial for maintaining portfolio performance in the volatile cryptocurrency market.

Methodology Overview

Building an optimized cryptocurrency portfolio using reinforcement learning-based Learning to Rank (LTR) requires a systematic approach that combines advanced machine learning techniques with financial portfolio theory. This methodology enables trading systems to dynamically adapt to market conditions, rank cryptocurrencies based on their potential, and optimize portfolio weights to maximize risk-adjusted returns.

The process involves collecting comprehensive cryptocurrency data, engineering relevant features, designing a reinforcement learning environment, training an LTR model, and implementing portfolio optimization strategies. By following this methodology, traders and investors can develop a data-driven approach to cryptocurrency portfolio management that balances risk and reward.

Key Components of the Methodology

The methodology consists of several interconnected components that work together to create a robust cryptocurrency portfolio optimization system:

- Data collection and preprocessing

- Feature engineering and selection

- Reinforcement learning environment design

- Learning to Rank (LTR) model implementation

- Portfolio construction and optimization

- Backtesting and performance evaluation

- Deployment and continuous improvement

Each component plays a crucial role in the overall effectiveness of the portfolio optimization strategy. The following sections will explore each component in detail.

Data Collection and Preprocessing

The foundation of any successful cryptocurrency portfolio optimization strategy is high-quality data. Collecting comprehensive and reliable data is essential for training effective models.

Types of Data to Collect

Market Data

Price data (OHLCV - Open, High, Low, Close, Volume) is fundamental for technical analysis and feature engineering. This data should be collected at various time intervals (e.g., 1-minute, 5-minute, 1-hour, 4-hour, daily) to capture both short-term and long-term patterns.

On-Chain Data

On-chain metrics provide insights into the actual usage and adoption of cryptocurrencies. Examples include transaction counts, active addresses, hash rates, and staking metrics. These metrics can offer valuable information about the health and growth potential of cryptocurrencies.

Market Sentiment Data

Sentiment analysis from social media, news articles, and forums can provide insights into market perception. Tools like sentiment analysis APIs, social media scraping, and news aggregation can be used to collect sentiment data.

Data Preprocessing

Once collected, the data needs to be preprocessed to ensure quality and consistency:

- Handling Missing Values: Cryptocurrencies may have gaps in their data history, especially newer coins. Techniques like forward-filling, interpolation, or more advanced imputation methods can be used to handle missing values.

- Normalization: Different features may have different scales. Normalizing the data ensures that all features contribute equally to the model.

- Time Series Alignment: Ensuring that all data points are properly aligned in time is crucial for accurate modeling.

- Outlier Detection and Handling: Extreme price movements and market manipulation can create outliers in the data. Robust normalization techniques or outlier removal methods can be applied.

Feature Engineering for Cryptocurrency Selection

Feature engineering transforms raw data into meaningful inputs for the reinforcement learning model. For cryptocurrency selection, we need to engineer features that capture various aspects of cryptocurrency performance and potential.

Technical Indicators

Technical indicators derive insights from historical price and volume data. Key technical indicators to consider include:

- Moving Averages: Simple Moving Average (SMA), Exponential Moving Average (EMA), and their crossovers

- Momentum Indicators: Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Stochastic Oscillator

- Volatility Indicators: Bollinger Bands, Average True Range (ATR), Historical Volatility

- Volume Indicators: On-Balance Volume (OBV), Volume-Weighted Average Price (VWAP), Accumulation/Distribution Line

On-Chain Metrics

On-chain metrics provide insights into the actual usage and adoption of cryptocurrencies:

- Network Activity: Transaction count, active addresses, transaction value

- Network Security: Hash rate, mining difficulty, staking metrics

- Token Economics: Supply distribution, token velocity, token unlock schedules

- DeFi Metrics: Total Value Locked (TVL), yield metrics, protocol revenue

Market Sentiment Features

Sentiment analysis can provide insights into market perception:

- Social Media Sentiment: Twitter, Reddit, Telegram sentiment scores

- News Sentiment: Sentiment analysis of cryptocurrency news articles

- Search Trends: Google Trends data for cryptocurrency-related search terms

- Community Metrics: GitHub activity, developer engagement metrics

Reinforcement Learning Environment Design

The reinforcement learning environment provides the framework for the agent to learn optimal trading strategies and portfolio weights. It should accurately simulate the cryptocurrency market dynamics and provide appropriate rewards for the agent's actions.

State Representation

The state representation should capture the relevant information about the current market conditions and portfolio status:

- Market Features: Technical indicators, on-chain metrics, sentiment features

- Portfolio State: Current holdings, cash position, portfolio value

- Historical Context: Past actions, performance, and market conditions

Action Space

The action space defines the possible actions that the agent can take:

- Position Strategy: Buy, sell, or hold decisions for each cryptocurrency

- Portfolio Weights: Allocation of capital among different cryptocurrencies

- Order Execution: Market orders, limit orders, stop orders

Reward Function

The reward function guides the agent towards optimal trading strategies and portfolio weights:

- Return-Based Rewards: Portfolio returns, excess returns over a benchmark

- Risk-Adjusted Rewards: Sharpe ratio, Sortino ratio, Calmar ratio

- Custom Objective Functions: Combining return, risk, and other objectives

| Reward Function Type | Formula | Advantages | Disadvantages |

|---|---|---|---|

| Portfolio Return | R = (P₁ - P₀) / P₀ | Simple, directly rewards profit | Does not account for risk |

| Sharpe Ratio | S = (R - Rᶠ) / σ | Rewards risk-adjusted returns | Assumes normal distribution of returns |

| Sortino Ratio | So = (R - Rᶠ) / σₚ | Only penalizes downside risk | More complex to implement |

| Custom Utility | U = w₁R - w₂σ - w₃C | Highly customizable | Sensitive to weight parameters |

Learning to Rank (LTR) Model Implementation

Learning to Rank (LTR) is a machine learning approach that focuses on ranking items based on their relevance or quality. In the context of cryptocurrency portfolio optimization, LTR can be used to rank cryptocurrencies based on their potential for future performance.

LTR Approach for Cryptocurrency Ranking

The LTR model takes the engineered features as input and produces a ranking of cryptocurrencies based on their expected performance:

- Pairwise Ranking: Compare pairs of cryptocurrencies to determine their relative ranking

- Listwise Ranking: Consider the entire list of cryptocurrencies when determining the ranking

- Pointwise Ranking: Assign a score to each cryptocurrency independently

Integration with Reinforcement Learning

The integration of LTR with reinforcement learning creates a powerful framework for cryptocurrency portfolio optimization:

- State Representation: LTR scores can be included in the state representation

- Action Selection: LTR rankings can guide the action selection process

- Reward Function: LTR performance can be incorporated into the reward function

Model Selection

Several reinforcement learning algorithms can be used for cryptocurrency portfolio optimization:

- Deep Q-Networks (DQN): Suitable for discrete action spaces

- Proximal Policy Optimization (PPO): Effective for continuous action spaces

- Soft Actor-Critic (SAC): Balances exploration and exploitation

- Twin Delayed DDPG (TD3): Reduces overestimation bias in value functions

This radar chart compares different reinforcement learning algorithms across multiple dimensions relevant to cryptocurrency portfolio optimization. The Soft Actor-Critic (SAC) algorithm excels in return optimization and adaptability, while Twin Delayed DDPG (TD3) offers superior risk management capabilities. DQN provides better computational efficiency and interpretability, making it suitable for environments with limited resources.

Portfolio Construction and Optimization

Once cryptocurrencies are ranked using the LTR model, the next step is to construct and optimize the portfolio based on these rankings.

Position Strategy

The position strategy determines when to enter or exit positions in specific cryptocurrencies:

- Entry Signals: Based on LTR rankings, technical indicators, and market conditions

- Exit Signals: Based on profit targets, stop-loss levels, and changing rankings

- Position Sizing: Determining the size of each position based on risk metrics and conviction

Portfolio Weight Optimization

Portfolio weight optimization allocates capital among the selected cryptocurrencies:

- Rank-Based Weighting: Allocate weights based on LTR rankings

- Mean-Variance Optimization: Optimize the portfolio based on expected returns and covariance matrix

- Kelly Criterion: Optimal bet sizing based on edge and probability of success

- Risk Parity: Allocate weights to equalize risk contribution from each asset

Risk Management

Effective risk management is crucial for long-term success in cryptocurrency trading:

- Diversification: Spreading investments across different cryptocurrencies and sectors

- Position Size Limits: Setting maximum position sizes to limit exposure to individual cryptocurrencies

- Stop-Loss Orders: Implementing stop-loss orders to limit potential losses

- Volatility-Based Sizing: Adjusting position sizes based on volatility

Conceptual Framework Visualization

The following mindmap illustrates the interconnected components of the reinforcement learning-based LTR methodology for cryptocurrency portfolio optimization. It provides a high-level overview of the key elements and their relationships within the framework.

This mindmap visualizes the comprehensive approach to cryptocurrency portfolio optimization using reinforcement learning and learning to rank. It highlights the interconnected nature of the various components, from data collection and feature engineering to model training, portfolio construction, and continuous evaluation.

Backtesting and Performance Evaluation

Backtesting is essential for evaluating the performance of the cryptocurrency portfolio optimization strategy before deploying it in live trading.

Backtesting Methodology

A robust backtesting methodology should simulate realistic trading conditions:

- Walk-Forward Testing: Train the model on historical data and test it on out-of-sample data

- Cross-Validation: Use techniques like k-fold cross-validation to ensure robust performance

- Transaction Costs: Include trading fees, slippage, and other transaction costs

- Liquidity Constraints: Consider market impact and liquidity limitations

Performance Metrics

Various metrics can be used to evaluate the performance of the portfolio optimization strategy:

- Return Metrics: Total return, annualized return, compound annual growth rate (CAGR)

- Risk Metrics: Volatility, maximum drawdown, Value at Risk (VaR)

- Risk-Adjusted Metrics: Sharpe ratio, Sortino ratio, Calmar ratio

- Relative Performance: Comparison to benchmarks like Bitcoin, Ethereum, or a cryptocurrency index

Implementation Insights: Video Tutorial

To help you better understand how to implement reinforcement learning strategies for cryptocurrency portfolio management, here's a video that provides valuable insights into the practical aspects of applying these techniques.

This video demonstrates how to build a reinforcement learning agent for trading cryptocurrencies and stocks. It covers the implementation details, challenges, and practical considerations for applying reinforcement learning to financial time series. The techniques discussed align well with our methodology and can serve as a practical guide for implementation.

Visual Examples of Cryptocurrency Data Analysis

Understanding the visual patterns in cryptocurrency data can provide insights for feature engineering and model development. Here are some examples of cryptocurrency data visualization that can inform your approach.

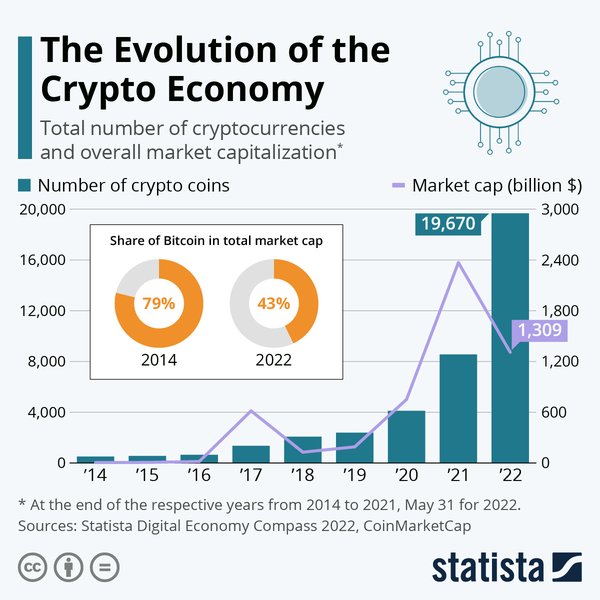

This chart illustrates the evolution of the cryptocurrency economy over time, showing how different segments have grown and evolved. Understanding these shifts can help inform your feature engineering and model design.

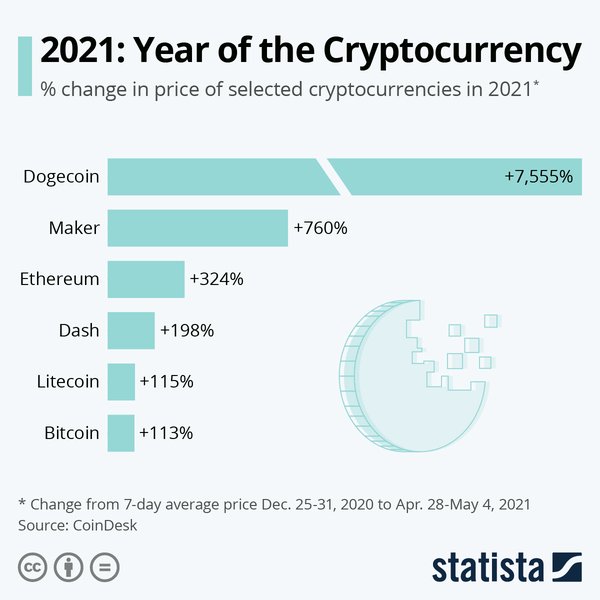

This visualization shows the price growth of various cryptocurrencies, highlighting the diverse performance across different assets. This diversity underscores the importance of an effective ranking and selection methodology.

Deployment and Continuous Improvement

Deploying the cryptocurrency portfolio optimization strategy involves setting up infrastructure for automated trading and continuous monitoring.

Deployment Infrastructure

The deployment infrastructure should support reliable and secure trading operations:

- API Integration: Integration with cryptocurrency exchanges for executing trades

- Data Pipeline: Automated data collection and preprocessing pipeline

- Monitoring System: Real-time monitoring of portfolio performance and market conditions

- Alert System: Notification system for significant events or anomalies

Continuous Improvement

The cryptocurrency market is dynamic and constantly evolving. Continuous improvement is essential for maintaining performance:

- Regular Retraining: Retrain the model periodically with new data

- Feature Evolution: Continuously evaluate and update the feature set

- Hyperparameter Optimization: Periodically optimize model hyperparameters

- Adaptive Learning Rate: Adjust the learning rate based on market conditions

ChatGPT Prompts for Python Code Implementation

The following prompts can be used to generate Python code for implementing the cryptocurrency portfolio optimization methodology. These prompts are designed to cover each component of the methodology in a modular fashion.

Data Collection and Preprocessing

# Prompt 1: Data Collection

Write a Python script to collect historical cryptocurrency data using the CCXT library. The script should collect OHLCV data for the top 20 cryptocurrencies by market capitalization from multiple exchanges. Include error handling and data validation.

# Prompt 2: Data Preprocessing

Create a Python function to preprocess cryptocurrency data. The function should handle missing values, normalize the data, align time series data, and detect outliers. Provide options for different normalization techniques and outlier detection methods.

Feature Engineering

# Prompt 3: Technical Indicators

Write a Python class to calculate technical indicators for cryptocurrency data. Include functions for moving averages (SMA, EMA), momentum indicators (RSI, MACD), volatility indicators (Bollinger Bands, ATR), and volume indicators (OBV, VWAP).

# Prompt 4: On-Chain Metrics

Create a Python script to collect and process on-chain metrics for cryptocurrencies using the Glassnode API. Include metrics such as active addresses, transaction counts, and network growth.

# Prompt 5: Sentiment Analysis

Develop a Python function to perform sentiment analysis on cryptocurrency-related social media data. Use the Twitter API to collect tweets and a pre-trained sentiment analysis model to calculate sentiment scores.

Reinforcement Learning Environment

# Prompt 6: RL Environment Setup

Create a reinforcement learning environment for cryptocurrency portfolio optimization using the Gym library. Define the state space, action space, and reward function. The environment should simulate trading multiple cryptocurrencies with realistic constraints.

# Prompt 7: State Representation

Write a Python function to encode the state representation for the reinforcement learning environment. The function should combine market features, portfolio state, and historical context into a comprehensive state representation.

# Prompt 8: Reward Function

Develop a custom reward function for the reinforcement learning environment that balances return maximization and risk minimization. Include options for different reward functions, such as Sharpe ratio, Sortino ratio, and custom utility functions.

Learning to Rank Model

# Prompt 9: LTR Model Implementation

Implement a Learning to Rank model for cryptocurrency selection using PyTorch. Choose a suitable architecture (e.g., a neural network with multiple layers) and loss function (e.g., pairwise ranking loss).

# Prompt 10: Training the LTR Model

Write a Python script to train the Learning to Rank model on historical cryptocurrency data. Include data splitting, model training, validation, and hyperparameter tuning.

# Prompt 11: RL-LTR Integration

Develop a Python class that integrates the Learning to Rank model with the reinforcement learning environment. The class should use the LTR model's rankings to inform the RL agent's decision-making process.

Portfolio Construction and Optimization

# Prompt 12: Position Strategy

Create a Python class for implementing position strategies based on LTR rankings. Include functions for generating entry and exit signals, setting stop-loss and take-profit levels, and managing position sizes.

# Prompt 13: Portfolio Weight Optimization

Implement a portfolio weight optimization algorithm in Python. Include options for rank-based weighting, mean-variance optimization, Kelly criterion, and risk parity.

# Prompt 14: Risk Management

Develop a Python class for risk management in cryptocurrency trading. Include functions for setting position size limits, implementing stop-loss orders, and dynamically adjusting position sizes based on volatility.

Backtesting and Evaluation

# Prompt 15: Backtesting Framework

Write a Python class for backtesting cryptocurrency trading strategies. The class should simulate trading with realistic assumptions about transaction costs, slippage, and market impact.

# Prompt 16: Performance Metrics

Implement a Python function to calculate performance metrics for a cryptocurrency portfolio. Include return metrics, risk metrics, risk-adjusted metrics, and relative performance compared to benchmarks.

# Prompt 17: Visualization

Create a Python script to visualize the backtesting results. Include plots of cumulative returns, drawdowns, performance metrics, and comparisons to benchmarks.

Deployment and Monitoring

# Prompt 18: Exchange API Integration

Implement a Python class for integrating with cryptocurrency exchange APIs. Include functions for retrieving account information, placing orders, and monitoring open positions.

# Prompt 19: Automated Trading System

Develop a Python script for an automated trading system that implements the cryptocurrency portfolio optimization strategy. The script should run continuously, collecting data, updating the model, and executing trades.

# Prompt 20: Monitoring Dashboard

Create a Python dashboard using Dash or Streamlit for monitoring the performance of the cryptocurrency portfolio optimization strategy. Include real-time performance metrics, portfolio composition, and alerts for significant events.

Frequently Asked Questions

References

- Cryptocurrency Portfolio Management with Deep Reinforcement Learning - ResearchGate

-

Reinforcement Learning for Cryptocurrency Portfolio Management - ScienceDirect

-

Deep Reinforcement Learning approach for Trading Cryptocurrencies - ScienceDirect

- Deep Reinforcement Learning for Financial Portfolio Management - arXiv

- A Deep Reinforcement Learning approach with Explainability for cryptocurrency trading - Eureka Select

- Scientists create a crypto portfolio management AI trained with on-chain data - CoinTelegraph

- Deep Reinforcement Learning for Trading Cryptocurrencies - Medium

Recommended Queries

Last updated April 5, 2025