Germany's Inflation Rate Revealed: Where Do Prices Stand Right Now?

An in-depth look at the latest inflation figures, trends, and economic context for Germany in early 2025.

Highlights: Germany's Inflation Snapshot (April 2025)

- Current Annual Rate: Preliminary data shows inflation at 2.1% year-over-year for April 2025, a slight decrease from 2.2% in March.

- Persistent Core Inflation: While headline inflation moderates, core inflation (excluding food and energy) remained higher at 2.6% in March 2025, indicating underlying price pressures.

- Gradual Easing Trend: Inflation continues its downward trend from the peaks seen in previous years, moving closer to the European Central Bank's target, although month-on-month price increases persist.

Unpacking the Numbers: Germany's Inflation in Detail

The Latest Annual Rate (April 2025)

As of the most recent data available (May 5, 2025), the provisional annual inflation rate in Germany stands at 2.1% for April 2025. This figure, calculated based on the year-on-year change in the Consumer Price Index (CPI), represents a slight easing compared to the previous month. The CPI tracks the average price changes for a basket of goods and services typically purchased by households.

Looking Back Slightly (March 2025)

The confirmed annual inflation rate for March 2025 was 2.2%. While the April figure shows a minor decrease, both rates indicate that prices are moderately higher than they were one year prior. This level of inflation, while significantly lower than the spikes experienced during the energy crisis of 2022-2023, still impacts consumer purchasing power.

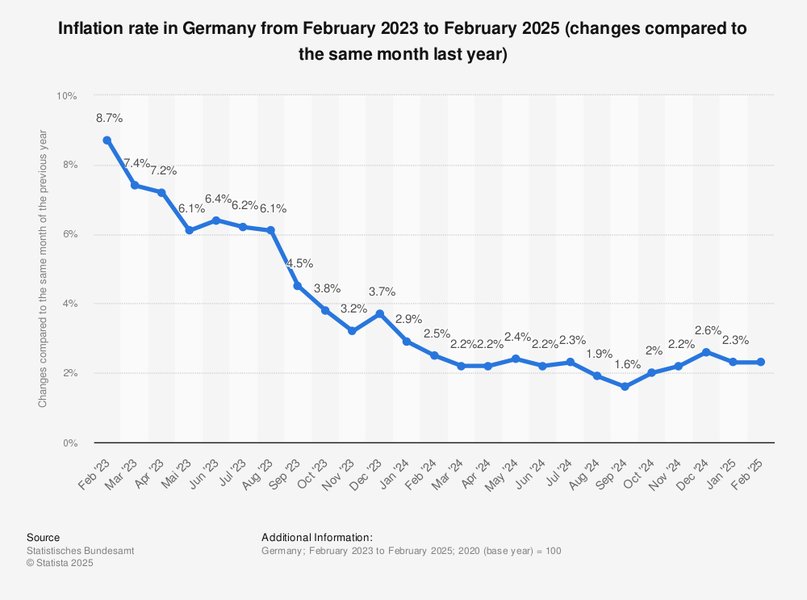

Recent year-over-year inflation rates in Germany.

Month-over-Month Price Changes

Examining shorter-term dynamics provides further insight. Consumer prices saw a month-over-month increase:

- From March 2025 to April 2025: +0.4%

- From February 2025 to March 2025: +0.3%

These monthly increases, particularly the slightly higher rate in April, suggest that while the annual rate is slowly decreasing, prices are still creeping upwards month by month, contributing to the overall annual figure.

Understanding Core Inflation

What is Core Inflation?

Core inflation is a crucial metric that strips out volatile components like energy and food prices from the overall inflation calculation. By excluding these items, which can experience significant short-term price swings, core inflation provides a clearer picture of underlying, more persistent inflationary trends within the economy, often driven by services and non-energy industrial goods.

Germany's Core Rate

In March 2025, Germany's core inflation rate stood at 2.6% year-on-year. This represented a decrease from 2.7% in February 2025 and marked the lowest level for core inflation since June 2021. While lower than headline inflation during the peak energy crisis, the fact that core inflation (2.6% in March) remained above the headline rate (2.2% in March) suggests that price pressures in less volatile sectors, particularly services, are still relatively strong and contributing significantly to the overall cost of living increases.

Recent Trends and Historical Context

The Downward Trajectory

Germany's inflation rate has been on a general downward path throughout late 2024 and into early 2025. After remaining above 3% in early 2024 and peaking significantly higher in 2022 (average 6.87%) and 2023 (average 5.95%), the current rates reflect a notable moderation. The rate decreased from 2.3% in February 2025 to 2.2% in March, and further to a provisional 2.1% in April.

Visualizing the trend of German inflation heading lower.

Comparison with Past Highs

The current inflation levels around 2.1-2.2% are substantially lower than the double-digit figures seen briefly during the height of the energy price surge following geopolitical events in 2022. This easing provides some relief to consumers and businesses but indicates that the inflationary period has left a lasting impact on price levels.

Long-Term Perspective

Historically, Germany's long-term average inflation rate (from 1950 to 2025) is around 2.49%. More recent averages, particularly using the Harmonized Index of Consumer Prices (HICP) relevant for EU comparisons (1996-2025), hover around 1.92%. The current rate of 2.1% is therefore slightly above the recent historical norm but closer to the longer-term average, suggesting a return towards more typical inflationary conditions, albeit still slightly elevated.

Key Factors Influencing Inflation

German inflation is influenced by a complex interplay of domestic and international factors. The following mindmap illustrates some of the primary drivers affecting current price levels:

As shown, factors ranging from global energy markets and ECB monetary policy to domestic wage pressures and consumer behavior all contribute to the final inflation figures. While energy price shocks have lessened compared to 2022/23, their residual effects and ongoing costs in areas like food and services continue to influence the overall rate.

Germany's Inflation in a Global Context

Understanding how Germany's inflation compares to its neighbors and other major economies provides valuable context.

Comparison with Euro Area

In April 2025, Germany's provisional inflation rate of 2.1% was slightly below the stable Euro Area average, which stood at 2.2% for the same period. This indicates that Germany's inflation dynamics are broadly aligned with the wider Eurozone trends, though currently marginally lower.

Comparison with Other Major Economies

Looking further afield:

- The United States reported an annual inflation rate of 2.4% as of March 2025.

- Switzerland experienced an unexpected drop in inflation, reaching 0% year-on-year in April 2025.

These comparisons highlight the varying economic conditions and policy responses across different countries.

Comparative Inflation Metrics Radar Chart

The following chart provides a visual comparison of key inflation indicators for Germany (April 2025), the Eurozone Average (April 2025 estimate), and the USA (March 2025 estimate), based on available data and reasonable estimations for illustrative purposes. Note that core rates and component changes may refer to slightly different periods (e.g., March) based on data availability.

This visualization helps compare the different facets of inflation across these economies. Germany currently shows slightly lower headline and core inflation compared to the estimated Eurozone average and US figures, though monthly price increases remain noticeable.

Recent Monthly Inflation Data Summary

The table below summarizes the key inflation metrics for Germany in the early months of 2025, illustrating the recent trend:

| Month (2025) | Annual CPI Rate (%) | Monthly Change (%) | Core Rate (%) |

|---|---|---|---|

| January | 2.3 | N/A | N/A |

| February | 2.3 | N/A | 2.7 |

| March | 2.2 | +0.3 | 2.6 |

| April | 2.1 (provisional) | +0.4 | Not yet available |

Note: N/A indicates data not explicitly cited for that metric in the source materials or not yet released. Core rate data often lags headline figures.

This table highlights the gradual decrease in the annual rate alongside persistent, albeit moderate, monthly price increases.

Economic Outlook and ECB Target

Government Forecasts and Economic Conditions

The persistence of inflation, even at these moderated levels, continues to influence the German economic outlook. Some analyses suggest that these ongoing price pressures contribute to forecasts of economic stagnation for Germany in 2025. While inflation has cooled significantly, its impact on consumer spending and business investment remains a key factor for economic performance.

Proximity to ECB Target

The European Central Bank (ECB) aims for inflation "below, but close to, 2%" over the medium term for the Eurozone. Germany's current rate of 2.1% is very close to this target ceiling. This proximity suggests that inflationary pressures are becoming more managed, potentially influencing future ECB monetary policy decisions, such as considerations around interest rates for the Eurozone as a whole.

Understanding Germany's Inflation Landscape

The following video provides additional context on understanding inflation dynamics specifically within Germany, discussing factors and impacts relevant to the current economic situation:

This video explores various aspects of inflation in Germany, offering insights into how current rates are perceived and managed within the country's economic framework.

Frequently Asked Questions (FAQ)

What is the latest official inflation figure for Germany?

How is inflation measured in Germany?

Is German inflation going up or down?

What is core inflation, and what is it currently in Germany?

How does Germany's inflation compare to the Eurozone average?

Recommended Reading

- What factors are driving German inflation in 2025?

- Explore the historical inflation trends in Germany over the last decade.

- How does the European Central Bank's monetary policy affect German inflation?

- Compare the cost of living changes in different German states due to inflation.

References

Last updated May 5, 2025