Unlocking Tax Deductions: The Key to Borrowing Costs on Collateralized Assets

Understanding how to strategically deduct borrowing costs when leveraging your assets is crucial for optimizing your financial position.

Key Insights into Borrowing Cost Deductibility

- Loan Purpose is Paramount: The primary factor determining whether borrowing costs are deductible is not the collateral itself, but how the loan proceeds are utilized. Funds used for business, taxable investments, or qualified home improvements generally qualify for deductions.

- Beyond Interest – Other Deductible Costs: Beyond just interest, certain other borrowing expenses like loan origination fees, mortgage points, and appraisal fees may also be deductible, often requiring amortization over the loan's term.

- "Buy, Borrow, Die" Strategy: High-net-worth individuals often use this strategy, borrowing against appreciating assets instead of selling them, to access capital without triggering immediate capital gains taxes, with potential for interest deductibility.

When you pledge assets as collateral for a loan, you might wonder if the associated borrowing costs, particularly interest, can be written off or deducted for tax purposes. The answer, often complex, hinges primarily on the "interest tracing rule" applied by tax authorities. This rule dictates that the deductibility of interest is determined by the *use* of the borrowed funds, not simply the fact that an asset has been pledged as security.

This comprehensive guide delves into the nuances of deducting borrowing costs on collateralized assets, exploring various scenarios, specific IRS guidelines, and strategic considerations to help you navigate this intricate area of tax law. The information presented reflects current tax guidelines as of June 1, 2025.

Understanding Borrowing Costs and the Role of Collateral

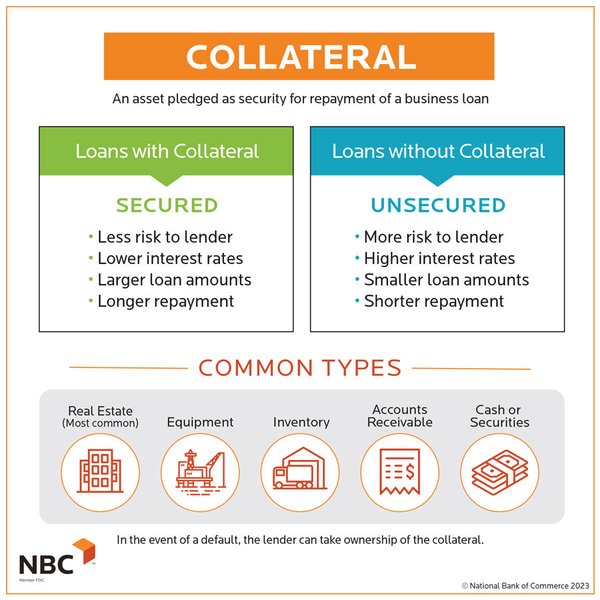

Borrowing costs encompass more than just the interest paid on a loan. They can include a range of fees and expenses incurred to secure the financing. When an asset like real estate, securities, or business equipment is used as collateral, it provides the lender with security, reducing their risk. However, this act of pledging an asset itself does not automatically grant tax deductibility for the associated borrowing costs.

What Constitutes Borrowing Costs?

Typically, borrowing costs can include:

- Loan interest payments

- Loan establishment or origination fees

- Mortgage broker fees

- Appraisal and legal fees related to securing the loan

- "Points" or prepaid interest

- Other specific expenses associated with obtaining the loan

The crucial distinction for tax purposes lies in the application of the loan proceeds. If the funds are deployed for income-producing activities or qualified purposes, the related borrowing costs may be deductible. Conversely, if the funds are used for personal consumption, the interest generally remains non-deductible.

This radar chart illustrates the typical deductibility potential and the complexity of tax rules across different uses of loan proceeds. Higher values indicate greater potential for deduction or higher complexity.

The Principle of Interest Tracing: How Loan Use Determines Deductibility

The core principle governing the deductibility of interest on collateralized loans is the "interest tracing" rule. This IRS guideline mandates that the tax treatment of the interest expense depends entirely on how the borrowed money is spent, rather than the type of asset pledged as collateral.

Business and Investment Purposes

If you borrow money and use the proceeds for business activities or to acquire taxable investments, the interest paid on that loan is generally deductible. This applies whether the collateral is business assets, securities, or even personal real estate, provided the funds are demonstrably used for income-generating purposes.

- Business Expenses and Capital Expenditures: Interest on loans used for general working capital, purchasing fixed assets for a business, or funding business growth is typically fully deductible as an ordinary and necessary business expense.

- Taxable Investments: Interest on loans used to purchase taxable investments (e.g., stocks, bonds, mutual funds that generate taxable income) can be deducted as an investment interest expense. This deduction is limited to your net investment income for the year, reported on IRS Form 4952.

- Rental Property Expenses: Borrowing costs associated with acquiring, improving, or maintaining a rental property, such as loan establishment fees, title search fees, and mortgage broker fees, are generally deductible. If the total borrowing expenses exceed $100, they are typically amortized over five years or the loan's term, whichever is shorter.

Business assets often serve as collateral for loans, and the interest on such loans can be deductible if the funds are used for business operations.

Home Mortgage Interest

For loans secured by your primary residence, specific rules apply. Interest on a home equity loan or a Home Equity Line of Credit (HELOC) is deductible only if the borrowed funds are used to buy, build, or substantially improve the taxpayer's home that secures the loan. For tax years 2018 through 2025, there is a limit on the total amount of acquisition indebtedness (including home equity loans) for which interest can be deducted, generally capped at $750,000 ($375,000 for married individuals filing separately).

Non-Deductible Scenarios

Conversely, certain uses of loan proceeds generally do not qualify for interest deductions, regardless of the collateral:

- Personal Loans: Interest on loans used for personal expenses (e.g., vacations, consumer goods, personal vehicle purchases) is typically not tax-deductible. This holds true even if the loan is secured by valuable collateral.

- Tax-Exempt Investments: A critical exception to the investment interest deduction rule is if the loan proceeds are used to purchase or carry tax-exempt investments (e.g., municipal bonds). In such cases, the interest on the loan is NOT deductible, as it prevents taxpayers from effectively creating a deduction for income that is already tax-exempt. This also applies if tax-exempt investments are used as collateral for the loan.

Navigating "Other" Borrowing Costs

Beyond recurring interest payments, other upfront borrowing costs can also be deductible, though their treatment often differs from interest. Many of these expenses must be amortized over the loan's life rather than being deducted entirely in the year they are paid.

| Cost Type | Deductibility Rules | Typical Treatment |

|---|---|---|

| Loan Interest | Deductible if loan proceeds used for business, taxable investment, or qualified home improvement. | Deducted annually as paid, or limited by net investment income. |

| Loan Origination Fees (Points) | Generally amortized over the loan term. May be immediately deductible for home acquisition/improvement. | Spread out over the life of the loan. |

| Mortgage Broker Fees | Amortized over the loan term for business/investment property. | Spread out over the life of the loan. |

| Appraisal & Legal Fees | For business/investment property, amortized over the loan term. | Spread out over the life of the loan. |

| Lender’s Mortgage Insurance (LMI) | For rental properties, amortized over 5 years or loan term. | Spread out over 5 years or loan term. |

This table summarizes the deductibility and typical treatment of various borrowing costs, highlighting whether they are immediately deductible or must be amortized.

Strategic Borrowing: The "Buy, Borrow, Die" Strategy

High-net-worth individuals often employ a strategy known as "Buy, Borrow, Die" to leverage appreciated assets without triggering immediate capital gains taxes. This strategy involves:

- Buy: Acquiring and holding appreciating assets, such as stocks, real estate, or business interests.

- Borrow: Taking out loans secured by these appreciating assets instead of selling them. The loan proceeds provide liquidity without a taxable event. The interest on these loans can often be deductible if used for taxable investment or business purposes.

- Die: Upon the death of the asset holder, the assets receive a "step-up in basis" to their fair market value on the date of death. This means heirs can inherit the assets and sell them with little to no capital gains tax, as their cost basis is effectively reset to the market value at the time of inheritance.

This strategy minimizes current tax liabilities by avoiding capital gains and potentially allows for interest deductions, while also providing a significant tax benefit for heirs. It is, however, complex and typically requires careful planning with tax and financial advisors.

Risks Associated with Collateralized Loans

While collateralized loans can offer benefits like lower interest rates and access to capital, they come with inherent risks:

- Collateral Calls: If the value of pledged securities or other assets declines significantly, lenders may issue a "collateral call," requiring you to provide additional collateral or repay a portion of the loan. Failure to do so can result in the forced sale of your pledged assets, potentially at an unfavorable time, which could trigger unexpected tax consequences (e.g., capital gains).

- Asset Unavailability: A significant portion of your assets may be tied up as collateral, limiting your liquidity and flexibility to use those assets for other purposes.

- Default Consequences: If you default on the loan, the lender has the right to seize and sell your collateral to recover their funds. This is considered a sale for tax purposes, and you would recognize a capital gain or loss based on the difference between the sale price and your original basis in the asset.

This mindmap illustrates the central concept that the deductibility of borrowing costs hinges on the use of loan proceeds, rather than merely the presence of collateral, along with specific scenarios and related considerations.

Youtube Video: How to Avoid Taxes Like The Rich - Buy Borrow Die Strategy

The "Buy, Borrow, Die" strategy is a sophisticated financial maneuver often employed by the wealthy to grow and transfer wealth efficiently while minimizing tax liabilities. This video elaborates on the core principles of this strategy, explaining how individuals can borrow against appreciating assets to access liquidity without triggering capital gains taxes, and how these assets can then be passed on to heirs with a stepped-up basis.

Understanding this strategy is highly relevant to the discussion of borrowing costs on collateralized assets because it demonstrates a powerful, tax-aware application of such loans. It highlights how the ability to borrow against assets (using them as collateral) allows for significant capital access while deferring or potentially eliminating capital gains taxes, with the added benefit of potentially deducting the interest on these loans if used for qualified purposes. This provides a practical, high-level example of how leveraging collateralized assets can be integrated into broader wealth management and tax planning objectives.

This video explains the "Buy, Borrow, Die" strategy, a key method for high-net-worth individuals to access capital through collateralized loans while deferring taxes.

Frequently Asked Questions (FAQ)

Conclusion

The ability to deduct borrowing costs on assets pledged as collateral is not an automatic entitlement, but rather a privilege contingent on the strategic use of the loan proceeds. The "interest tracing" rule is paramount: if the borrowed funds are channeled into business operations, taxable investments, or qualified home improvements, the associated interest and other borrowing costs may indeed be deductible. However, using collateralized loans for personal expenses or to acquire tax-exempt investments will generally not yield a tax deduction for the interest paid. Understanding these distinctions, along with the nuances of amortizing various borrowing fees and the risks inherent in collateralized lending, is crucial for optimizing your financial and tax planning. Consulting a qualified tax professional is always recommended to ensure compliance and maximize legitimate deductions tailored to your specific financial circumstances.

Recommended Queries for Deeper Insights

- Understanding IRS Form 4952 and investment interest deduction

- Tax implications of securities-backed lines of credit

- Rules for deducting home equity loan interest for home improvements

- Amortization of loan origination fees for tax purposes