Unveiling Advanced Deep Learning Techniques for Modern Trading Bots

Exploring the Sophisticated Algorithms Driving Automated Financial Decisions

The landscape of financial trading has been profoundly transformed by the advent of artificial intelligence, particularly through the application of advanced deep learning techniques. Trading bots leveraging these methods can analyze vast amounts of market data, identify complex patterns, and execute trades with speed and precision far beyond human capabilities. This integration of AI into algorithmic trading aims to enhance efficiency, improve accuracy, and potentially uncover profitable opportunities in dynamic markets like stocks and cryptocurrencies.

Key Insights into Deep Learning for Trading Bots

- Neural Networks are Foundational: Deep learning techniques, often built upon sophisticated neural network architectures like LSTMs and Deep Neural Networks (DNNs), are crucial for processing sequential financial data and predicting market movements.

- Reinforcement Learning for Action Selection: Deep Reinforcement Learning (DRL) offers a powerful paradigm where trading bots learn optimal action sequences (buy, sell, hold) by interacting with the market environment and optimizing a defined reward function.

- Data is Paramount: The success of any deep learning trading bot heavily relies on access to high-quality, comprehensive, and properly preprocessed financial data, ranging from historical prices and volumes to alternative data sources.

The Role of AI and Machine Learning in Algorithmic Trading

Algorithmic trading, the process of executing orders using automated pre-programmed trading instructions accounting for variables such as time, price, and volume, is not new. However, the incorporation of Artificial Intelligence (AI) and Machine Learning (ML) has brought a new level of sophistication. AI trading strategies use algorithms to analyze data, learn from it, and improve trading decisions autonomously. This enhances efficiency and accuracy in the stock market and other financial markets.

Machine learning models, including techniques beyond deep learning like support vector machines (SVM), are used in AI trading to analyze historical data and predict market trends. They can process vast datasets in real-time, identify subtle patterns that might escape human traders, and make data-driven decisions without succumbing to emotional biases.

AI enhances various aspects of algorithmic trading, including:

Real-Time Data Analysis

AI systems can rapidly process incoming market data, news, and other relevant information streams simultaneously.

Improved Market Prediction Models

Advanced ML and DL models can build more complex and potentially more accurate predictive models compared to traditional statistical methods.

Optimised Trade Execution

AI can determine the optimal timing and size for trade execution to minimize impact costs and maximize returns based on current market conditions.

Minimizing Human Bias

By automating decisions based on data and learned patterns, AI helps eliminate emotional and cognitive biases that can negatively impact trading performance.

Advanced Risk Management

AI models can assess and manage risk dynamically by analyzing market volatility, potential drawdowns, and correlations across assets.

Deep Learning Techniques in Detail

Deep learning, a subset of machine learning that uses artificial neural networks with multiple layers, is particularly well-suited for handling complex, non-linear patterns often found in financial time series data. Unlike simpler models, deep learning architectures can automatically learn hierarchical representations of features from raw data.

Neural Networks: The Foundation

Artificial Neural Networks (ANNs) are computational models inspired by the structure and function of biological neural networks. They consist of interconnected nodes (neurons) organized in layers: an input layer, one or more hidden layers, and an output layer. "Deep" refers to the presence of multiple hidden layers, enabling the network to learn increasingly abstract representations of the input data.

An illustration depicting an AI trading bot analyzing cryptocurrency data.

Neural networks are state-of-the-art in computer science and are essentially trainable algorithms that try to emulate certain aspects of the human brain for tasks like pattern recognition and prediction. For trading, they are used to develop strategies based on an overall investment approach, whether it's focused on high-risk growth or more conservative long-term gains.

Types of Neural Networks for Trading

- Feedforward Neural Networks (DNNs): The simplest type, where information flows in only one direction, from input to output. Deep Multi-Layer Perceptrons (MLPs) are commonly used for predicting buy-sell-hold points based on optimized technical indicators.

- Recurrent Neural Networks (RNNs) and LSTMs: These networks are designed to process sequential data by having connections that form directed cycles, allowing them to maintain an internal memory. Long Short-Term Memory (LSTM) networks are a specific type of RNN particularly effective at learning from and predicting based on time series data, which is crucial for stock price forecasting where past sequence matters. LSTMs can capture long-term dependencies in data, which is vital for financial time series.

- Convolutional Neural Networks (CNNs): While primarily known for image processing, CNNs can also be applied to financial data by treating time series segments as 1D "images," useful for identifying specific local patterns.

- Stochastic Neural Networks: These incorporate stochastic behavior to model the inherent randomness and uncertainty in financial markets.

Training neural networks for trading involves feeding them large datasets of historical market information. The network learns to map input features (like price, volume, technical indicators, news sentiment) to desired outputs (like future price direction or volatility). However, a significant challenge with neural networks in finance is overfitting – where the model performs exceptionally well on historical training data but fails to generalize to new, unseen market conditions. Proper data preprocessing, validation, and regularization techniques are essential to mitigate overfitting.

Deep Reinforcement Learning (DRL) for Trading Actions

While supervised learning models like LSTMs can predict future values or directions, Deep Reinforcement Learning (DRL) offers a different paradigm: learning a policy that dictates a sequence of actions (buy, sell, hold) to maximize a cumulative reward. In DRL, an "agent" (the trading bot) interacts with an "environment" (the financial market). The agent observes the current "state" (market data), selects an "action" based on its policy, receives a "reward" (profit/loss, Sharpe ratio, etc.), and transitions to a new state. The goal is to learn a policy that yields the highest expected future rewards.

While not directly applied as commonly as CNNs or LSTMs in trading, the complexity of financial data can sometimes benefit from graph structures and related neural networks.

Deep Q-Learning is a popular DRL technique used in building trading bots. It combines Q-learning (a reinforcement learning algorithm) with deep neural networks to estimate the optimal action-value function. This function represents the expected future reward of taking a specific action in a given state.

The actions in a DRL trading bot are typically discrete: Buy, Sell, or Hold. The state is often represented by historical price data, technical indicators, or other relevant market information within a defined time window. The reward function is critical; it defines what the agent is trying to maximize. A simple reward could be the change in portfolio value after an action. More complex reward functions might incorporate risk-adjusted returns or penalize volatility.

The objective is not just to predict price movements but to learn the optimal *strategy* for interacting with the market to maximize profit, potentially under real market conditions like transaction costs.

Conceptual structure of a DRL trading agent:

# Conceptual outline of a DRL Trading Agent

Initialize Agent with Policy Network and Value Network (DNNs)

Define Market Environment (State, Actions, Reward)

Set Hyperparameters (Learning rate, Discount factor, etc.)

For each Trading Episode (e.g., a day or a week):

Reset Environment to initial state

While episode not finished:

Observe current State

Select Action (Buy, Sell, or Hold) based on Policy Network (e.g., using exploration/exploitation strategy)

Execute Action in Environment

Observe next State and immediate Reward

Store (State, Action, Reward, next State) in Replay Buffer

Sample a batch from Replay Buffer

Train Policy and Value Networks using sampled batch

Update Target Networks

Evaluate Agent performance periodically

DRL agents learn through trial and error, experiencing different market scenarios and refining their policy based on the rewards received. This makes them potentially more adaptable to changing market conditions compared to models that only predict prices.

Building and Deploying Deep Learning Trading Bots

Creating a deep learning trading bot involves several critical steps:

1. Data Collection and Preprocessing

This is the foundational step. High-quality historical data (prices, volumes, indicators) is essential. For advanced bots, alternative data like news sentiment, social media trends, or satellite imagery can also be incorporated. Data needs to be cleaned, handled for missing values, and normalized. Normalization, scaling data to a specific range (e.g., 0 to 1), is crucial as many stocks have seen large price swings, and neural networks learn better from scaled data, preventing higher values from dominating the learning process.

2. Model Development

Selecting and designing the appropriate deep learning architecture (LSTM, DNN, DRL agent) based on the trading strategy and the nature of the data. This involves defining the network layers, activation functions, and the output layer structure (e.g., predicting price change, predicting buy/sell/hold signal, or outputting action probabilities for DRL).

3. Training the Model

The deep learning model is trained on historical data using optimization algorithms (like Adam or SGD) to minimize a defined loss function (e.g., mean squared error for regression, cross-entropy for classification, or the policy/value loss for DRL). This step requires significant computational resources and time, especially with large datasets and complex models.

4. Backtesting

Before deploying the bot with real money, it must be rigorously backtested on historical data it has not seen during training. This simulates how the strategy would have performed in the past. Comprehensive backtesting platforms allow for simulating transaction costs, slippage, and other real-world market conditions to get a realistic estimate of potential performance. Metrics like Sharpe Ratio, maximum drawdown, and profitability are crucial for evaluation.

5. Optimization and Refinement

Based on backtesting results, the model parameters, network architecture, features, and strategy rules are refined. This iterative process aims to improve performance and robustness. Techniques like hyperparameter tuning and cross-validation are used.

6. Deployment and Monitoring

Once the strategy is backtested and refined, it can be deployed in a live trading environment. This involves connecting the bot to a brokerage or exchange API. Continuous monitoring of the bot's performance is essential, as market conditions can change, potentially degrading the model's effectiveness over time. Strategies may need periodic retraining or adaptation.

Specific Advanced Strategies and Applications

Deep learning enables the implementation of sophisticated trading strategies:

Pattern Recognition

Neural networks excel at identifying complex patterns in price charts and indicator movements that are difficult to define with fixed rules. Training a pattern recognition network involves feeding it examples of specific patterns and teaching it to classify future occurrences.

Enhancing Technical Analysis

Instead of simply using standard technical indicators, deep learning can learn how different indicators interact or predict outcomes under varying market regimes. For example, a neural network could be trained to forecast indicator movements or learn when traditional signals are more or less reliable.

Time Series Forecasting

Using LSTMs or other RNN variants to predict future price movements, volatility, or other time-dependent variables based on historical sequences. This requires careful handling of time series properties like stationarity and autocorrelation.

Sentiment Analysis Integration

Deep learning models, particularly those using Natural Language Processing (NLP) techniques like transformers, can analyze news headlines, social media posts, and other text data to gauge market sentiment and incorporate it into trading decisions.

Arbitrage Strategies

Identifying and exploiting small price differences for the same asset across different markets or exchanges. Deep learning can help identify these fleeting opportunities faster and more accurately.

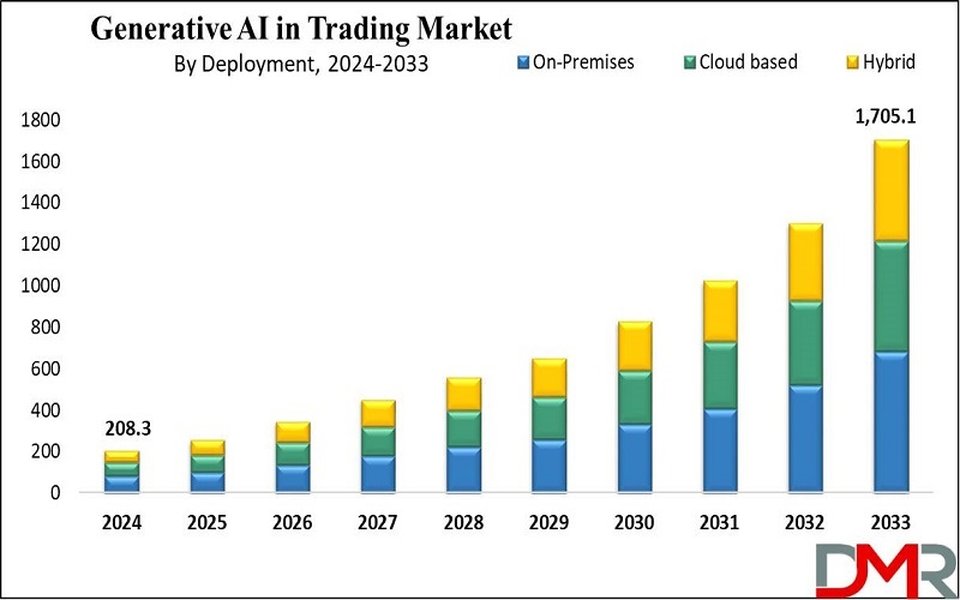

Market analysis indicating the expected growth in the Generative AI in Trading Market.

Deep Learning Techniques Summary

The table below summarizes some key deep learning techniques discussed and their applications in trading bots:

| Technique | Description | Primary Application in Trading | Benefits | Challenges |

|---|---|---|---|---|

| Deep Neural Networks (DNN / MLP) | Feedforward networks with multiple hidden layers. | Pattern recognition, signal generation from indicators, classification (Buy/Sell/Hold). | Learns complex non-linear relationships, relatively simpler to implement than RNNs for non-sequential data. | May struggle with time-dependent patterns, prone to overfitting without proper regularization. |

| Recurrent Neural Networks (RNN / LSTM) | Networks with internal memory loops, specialized LSTMs handle long-term dependencies. | Time series forecasting (prices, volatility), sequential pattern recognition. | Excellent at modeling sequential data, captures historical context. | Can be computationally expensive, complex to train, LSTMs help but training long sequences is still challenging. |

| Deep Reinforcement Learning (DRL) | Agent learns optimal actions through interaction with the environment and maximizing cumulative reward. | Learning optimal trading policies (sequence of Buy/Sell/Hold decisions), dynamic strategy adaptation. | Learns strategies directly from market interaction, can potentially adapt to changing conditions, handles sequential decision making. | Requires careful environment design and reward function definition, training can be unstable, sample efficiency can be low. |

Platforms and Tools

While building a custom deep learning trading bot requires significant technical expertise, various platforms and tools facilitate the process:

- MetaTrader 5 (MQL5): Allows development of trading robots (Expert Advisors) using MQL5, and integrating neural networks into these robots is possible with dedicated libraries or custom implementations.

- TrendSpider: Offers an AI Strategy Lab that allows traders to train custom AI-based strategies, focusing on pattern recognition and backtesting without requiring deep programming knowledge.

- Trade Ideas: Utilizes AI-generated algorithms (like the HOLLY AI system) to scan the market for trading opportunities and suggest strategies.

- Capitalise.ai: Provides a code-free platform to create, test, and automate trading scenarios using everyday English instructions, often powered by underlying AI logic.

- LevelFields AI, Tickeron, SignalStack: Other platforms offering AI-powered tools for market analysis, trade ideas, and automation signals.

- Programming Libraries (Python): Libraries like TensorFlow, Keras, PyTorch, and scikit-learn are essential for building custom deep learning models in Python, a popular language for quantitative trading.

Challenges and Considerations

Despite the potential, using deep learning for trading bots presents challenges:

-

Data Requirements: Deep learning models are data-hungry. Access to large, clean, and relevant historical data is crucial.

-

Overfitting: The risk of models performing well on historical data but failing in live trading due to capturing noise rather than signal.

-

Computational Cost: Training complex deep learning models can be computationally intensive and require powerful hardware.

-

Market Dynamics: Financial markets are non-stationary; patterns and relationships can change over time, requiring models to be continuously monitored and potentially retrained.

-

Interpretability: Deep learning models can be "black boxes," making it difficult to understand why a specific decision was made, which can be a challenge for strategy validation and debugging.

-

Transaction Costs and Slippage: Real-world trading involves costs and execution uncertainties that need to be properly accounted for in backtesting and live trading.

Further Exploration

To understand the practical application of these techniques, watching demonstrations of building such systems can be insightful. The following video provides a look into creating a day trading AI using a deep neural network.

This video demonstrates the process of creating a day trading AI using a deep neural network, offering a practical perspective on the concepts discussed, including data preparation, model building, and training. It helps visualize how deep learning is applied in building automated trading systems.

Frequently Asked Questions

What is the difference between algorithmic trading, machine learning, and deep learning in this context?

Algorithmic trading is the broad term for using computer programs to execute trades based on predefined rules. Machine Learning is a subset of AI that enables systems to learn from data without being explicitly programmed. Deep Learning is a subset of Machine Learning that uses multi-layered neural networks to learn complex patterns from data, often performing well on tasks like pattern recognition and sequence prediction.

Are deep learning trading bots consistently profitable?

There is no guarantee of consistent profit. While deep learning can identify complex patterns and automate trading, success depends heavily on the quality of the data, the strategy designed, proper implementation, risk management, and the dynamic nature of the market. Many factors can lead to underperformance, including overfitting, changing market conditions, and transaction costs.

What data is needed to train a deep learning trading bot?

Typically, historical market data like open, high, low, close prices, and volume are used. Technical indicators derived from this data are also common inputs. More advanced bots may incorporate alternative data sources such as news sentiment, economic indicators, or even satellite imagery depending on the strategy.

What is backtesting, and why is it important?

Backtesting is the process of testing a trading strategy on historical data to see how it would have performed. It is crucial for evaluating the potential effectiveness of a deep learning model before risking real capital. Robust backtesting helps identify potential flaws, estimate expected returns and risks, and compare different strategies.

What programming languages and libraries are commonly used?

Python is widely used due to its extensive ecosystem of libraries for data science and machine learning (TensorFlow, Keras, PyTorch, scikit-learn, Pandas, NumPy). MQL5 is the language used for developing Expert Advisors on the MetaTrader 5 platform.

Can I build a deep learning trading bot without extensive coding knowledge?

While building highly customized bots often requires coding, platforms like TrendSpider and Capitalise.ai offer interfaces that allow users to create and automate strategies using visual tools or natural language, abstracting away some of the underlying coding complexity.

References

Last updated April 18, 2025