Unlocking Dividend Reporting: Where Do They Fit in Your Company's Financial Story?

A clear guide to understanding how dividends are precisely accounted for across various financial statements.

When a company decides to share its profits with shareholders through dividends, specific accounting rules dictate how these distributions are recorded. Understanding this process is crucial for interpreting the financial health and policies of a business. Let's explore precisely where dividends make their mark on the financial reports.

Key Insights: Dividend Reporting at a Glance

- Equity Impact: Dividends directly reduce a company's retained earnings, a component of equity. This reduction is prominently featured in the Statement of Changes in Equity.

- Liability Recognition: Once declared but before payment, dividends become a short-term obligation. They are reported as "Dividends Payable" under current liabilities on the Statement of Financial Position (Balance Sheet).

- Transparency Through Notes: Detailed information about dividend policies, amounts per share, and declaration dates are typically disclosed in the notes accompanying the financial statements, offering crucial context.

Evaluating Dividend Reporting Options

You've asked which of the following statements accurately describe how dividends are reported. Let's break them down:

1. Charged to the Profit and Loss Account (Income Statement)

Status: Incorrect

Dividends are not considered an operating expense incurred in generating revenue. Therefore, they are not charged to the Profit and Loss Account (P&L), also known as the Income Statement. The P&L statement focuses on a company's operational performance (revenues and expenses) to arrive at net income or profit. Dividends are a distribution of these accumulated profits (retained earnings) to shareholders, not a cost of doing business. While dividends on preferred stock might sometimes be shown as a deduction from net income to calculate earnings available to common shareholders, they are not classified as a general expense item within the P&L itself.

2. Charged to the Statement of Changes in Equity

Status: Correct

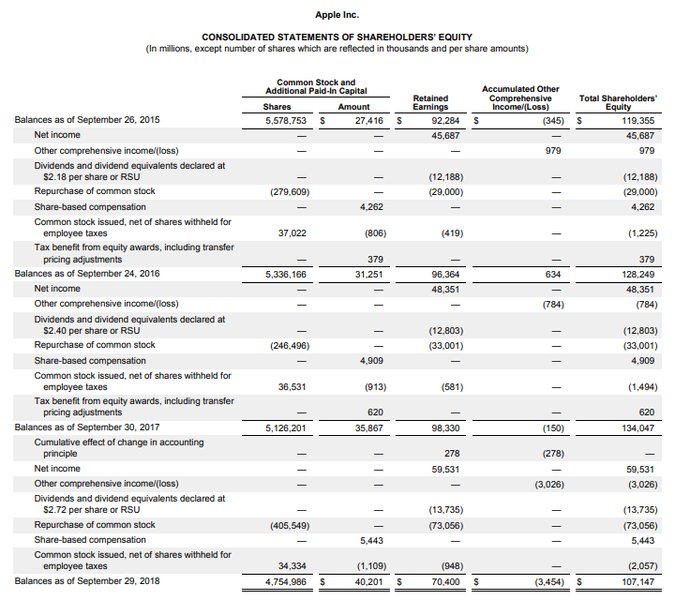

This is a primary location for dividend reporting. The Statement of Changes in Equity (sometimes called the Statement of Stockholders' Equity or Statement of Retained Earnings) details the movements in a company's equity accounts over a reporting period. Since dividends are paid out of retained earnings (which is a component of equity), their declaration and payment directly reduce retained earnings. This reduction is clearly shown in this statement, providing a transparent view of how profit distributions affect the company's overall equity.

An illustrative example of Apple Inc.'s Statement of Changes in Equity, where dividends paid would typically be shown as a deduction from retained earnings.

3. Charged to the Statement of Financial Position Under Current Liabilities

Status: Correct (Conditional)

This is correct, but with an important condition: dividends are reported as a current liability on the Statement of Financial Position (Balance Sheet) only after they have been declared by the company's board of directors but before they have been paid to shareholders. Once declared, the company has a legal obligation to pay the shareholders, making it a liability. This is typically recorded in an account called "Dividends Payable" under the current liabilities section because they are usually due within the next operating cycle (typically one year). Once the dividend is actually paid, the cash balance decreases, and the "Dividends Payable" liability is removed from the balance sheet.

4. Included as a Note Under the Notes Section of the Reports

Status: Correct

The notes to the financial statements provide additional detail and context to the figures presented in the main statements. Information regarding dividends is frequently disclosed here. These disclosures can include:

- The amount of dividends declared per share.

- The total amount of dividends declared and paid during the period.

- The dividend policy of the company.

- Key dates related to dividend declaration, record, and payment.

- Details about any restrictions on retained earnings that might affect dividend payments.

Comprehensive Overview of Dividend Accounting

The journey of a dividend through a company's financial reporting system involves several key statements. Understanding this flow provides a holistic view of its financial impact.

The Dividend Declaration and Payment Process

Reporting dividends typically involves two main accounting events:

- Declaration Date: On this date, the company's Board of Directors formally approves (declares) the dividend. At this point:

- Retained Earnings (Equity) is debited (decreased).

- Dividends Payable (Current Liability) is credited (increased).

- Payment Date: On this date, the company distributes the cash to shareholders. The accounting entry is:

- Dividends Payable (Current Liability) is debited (decreased).

- Cash (Current Asset) is credited (decreased).

Notice that the Income Statement is not directly impacted by these transactions. The profit has already been earned and recorded; dividends are simply a distribution of those accumulated earnings.

Dividend Impact Across Financial Statements: A Summary

The following table summarizes where and how dividends typically affect the primary financial statements:

| Financial Statement | Impact of Dividends | Explanation |

|---|---|---|

| Income Statement (Profit & Loss Account) | Generally No Direct Impact | Dividends are a distribution of profit, not an expense incurred to generate revenue. |

| Statement of Changes in Equity | Reduction in Retained Earnings | Shows the decrease in equity due to dividends distributed to shareholders. |

| Statement of Financial Position (Balance Sheet) | Increase in Current Liabilities (as Dividends Payable) when declared but unpaid. Decrease in Cash and elimination of Dividends Payable upon payment. | Reflects the obligation to pay (initially) and the subsequent outflow of cash. |

| Statement of Cash Flows | Outflow in Financing Activities | Cash dividends paid are reported as a use of cash within the financing activities section. This shows how the company uses its cash to return value to shareholders. |

| Notes to the Financial Statements | Detailed Disclosure | Provides supplementary information like dividend per share, total dividends, and dividend policy. |

Visualizing Dividend Reporting Complexity

To better understand the multifaceted impact of dividend reporting, consider the relative importance and nature of their appearance on different financial statements. The radar chart below illustrates how various aspects of financial reporting are affected by dividend declarations and payments. The scale indicates the degree of direct impact or disclosure prominence, from 1 (minimal/indirect) to 5 (significant/direct).

This chart highlights that cash dividends have a strong, direct impact on equity, liabilities (when unpaid), and cash flows, with minimal direct impact on the income statement as an expense, and significant disclosure in the notes. Stock dividends, while still affecting equity and requiring disclosure, have a different profile, particularly concerning cash flow and immediate liability creation.

Mapping Dividend Reporting Across Financial Statements

The mindmap below offers a visual summary of how dividend reporting is interconnected across the primary financial statements. It helps illustrate the journey of dividend information from declaration to its final reflection in the company's reported financials.

This mindmap visually organizes the key areas where dividends are reported, reinforcing that they are primarily an equity transaction and a financing cash outflow, rather than an operating expense.

Understanding Dividend Accounting: A Video Explainer

For a more dynamic explanation of how dividends are treated in financial statements, the following video provides a concise overview. It touches upon where dividends appear, such as the balance sheet (as "dividends payable") and clarifies why they are not found in the company's income statement.

This video explains where to find dividends in financial statements, highlighting their absence from the income statement and presence on the balance sheet as "dividends payable" when declared but not yet paid.

Watching this can help solidify the concepts discussed, particularly the distinction between equity distributions and operational expenses.

Frequently Asked Questions (FAQ)

Recommended Further Exploration

- How does the declaration of dividends affect a company's working capital?

- What are the implications of a company consistently paying high dividends?

- Explain the differences in accounting for cash dividends versus stock dividends in detail.

- How do dividend reinvestment plans (DRIPs) get reflected in financial reporting for both the company and the investor?

References

assets.kpmg.com

assets.kpmg.com

Last updated May 6, 2025