Essential Best Practices for Ensuring Comprehensive Homeowners Insurance Coverage

Protect your home and assets with these expert-recommended strategies

Key Takeaways

- Accurate Coverage Assessment: Regularly evaluate and adjust your policy to reflect the true value of your home and possessions.

- Comprehensive Policy Understanding: Familiarize yourself with all aspects of your policy, including coverage types, exclusions, and additional endorsements.

- Proactive Risk Management: Implement safety measures and maintain your property to reduce risks and potentially lower insurance premiums.

1. Accurately Assess Your Coverage Needs

Ensure your policy reflects the true value of your home and belongings

Begin by determining the replacement cost of your home, which includes labor and materials required to rebuild it in its current state. This is not the same as the market value, which can fluctuate based on real estate trends. Use local construction costs to calculate an accurate estimate. Additionally, create a detailed inventory of your personal belongings, accounting for high-value items such as jewelry, electronics, and antiques. Consider using inventory apps or templates to document these items with photos and receipts, ensuring they are fully covered under your policy.

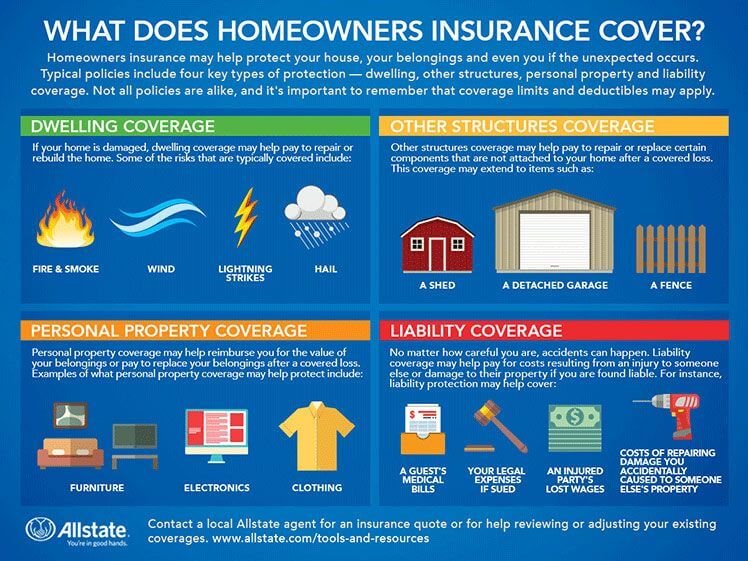

2. Understand Your Policy Components

Familiarize yourself with coverage types, exclusions, and endorsements

Homeowners insurance policies typically include several key components:

- Dwelling Coverage: Protects the physical structure of your home against covered perils like fire, windstorm, and vandalism.

- Personal Property Coverage: Covers your personal items within the home. Ensure it is sufficient, typically 50-70% of your dwelling coverage.

- Liability Coverage: Protects against lawsuits for bodily injury or property damage you or family members cause to others.

- Additional Living Expenses (ALE): Covers costs if your home becomes uninhabitable due to a covered event.

Understand the difference between Actual Cash Value (ACV) and Replacement Cost Coverage. ACV accounts for depreciation, while Replacement Cost Coverage reimburses the cost to replace items without depreciation. Opt for Replacement Cost Coverage to ensure full reimbursement.

3. Regularly Review and Update Your Policy

Keep your coverage aligned with changes in your home and personal circumstances

Life changes such as home renovations, purchasing expensive items, or changes in local building costs can impact your insurance needs. Schedule annual reviews of your policy to adjust coverage limits accordingly. Update your insurer promptly after making significant home improvements or acquiring high-value possessions to ensure they are adequately covered. Implement an inflation guard clause if available, which automatically adjusts your coverage limits to keep up with rising construction and labor costs.

4. Choose the Right Deductible

Balance between affordable premiums and manageable out-of-pocket expenses

The deductible is the amount you pay out of pocket before your insurance coverage kicks in. Selecting a higher deductible can lower your premium payments, but it means you'll bear more cost in the event of a claim. Assess your financial situation to determine a deductible that balances affordability with your ability to cover unexpected expenses.

5. Bundle Policies for Cost Savings

Combine multiple insurance policies to receive discounts and simplify management

Many insurance providers offer discounts when you bundle your homeowners insurance with other policies, such as auto or life insurance. Bundling not only reduces your overall premium costs but also streamlines your insurance management by consolidating policies with a single provider.

6. Enhance Home Security and Safety Features

Implement measures to reduce risks and potentially lower your insurance premiums

Installing security systems, smoke detectors, and storm shutters can significantly reduce the risk of damage to your home and may qualify you for insurance discounts. Regular maintenance of critical systems like roofing, plumbing, and electrical can prevent issues that might lead to insurance claims or policy cancellations due to neglect.

7. Shop Around and Compare Insurance Quotes

Evaluate multiple insurers to find the best coverage at competitive prices

Obtaining quotes from various insurance companies allows you to compare coverage options, exclusions, deductibles, and premiums. Use online comparison tools or consult with independent insurance agents to identify the most suitable policy. Ensure that you compare not just premiums but also customer service ratings and claims handling efficiency.

8. Understand Policy Exclusions and Add Necessary Endorsements

Be aware of what your policy does not cover and seek additional protection as needed

Standard homeowners policies may exclude certain risks such as floods, earthquakes, or mold damage. Assess whether these exclusions apply to your situation based on your geographic location and lifestyle. Purchase additional riders or separate policies to cover these specific perils if necessary. For example, flood insurance might be essential if your home is in a flood-prone area.

9. Maintain a Detailed Documentation of Your Home and Belongings

Streamline the claims process by keeping thorough records

Maintain an up-to-date inventory of your possessions, including photographs, receipts, and detailed descriptions. This documentation facilitates the claims process by providing clear evidence of your assets' value. Store this information securely, both digitally and physically, to ensure accessibility in case of a loss.

10. Seek Guidance from Reputable Insurance Professionals

Consult with experts to tailor your policy to your specific needs

Working with a knowledgeable insurance agent or financial advisor can help you navigate the complexities of homeowners insurance. These professionals can assess your unique risks, recommend appropriate coverage levels, and identify potential discounts. They can also assist in interpreting policy language to ensure you fully understand your coverage.

11. Implement Risk Assessment and Prevention Strategies

Proactively manage risks to enhance home safety and reduce insurance costs

Regularly assess potential risks to your home, such as fire hazards, water leaks, or structural vulnerabilities. Implement preventive measures like installing sprinkler systems, regular roof inspections, and updating outdated electrical wiring. Proactive maintenance not only safeguards your home but may also make you eligible for lower insurance premiums.

12. Review and Utilize Policy Inflation Protection

Ensure your coverage keeps up with rising costs over time

Inflation can erode the value of your coverage over time, leading to insufficient protection. An inflation guard clause automatically adjusts your coverage limits annually based on inflation rates, ensuring that your policy remains adequate to cover increased rebuilding costs and replacement expenses without requiring manual updates.

Conclusion

Ensuring that your homeowners insurance policy provides comprehensive coverage requires a proactive and informed approach. By accurately assessing your coverage needs, understanding the various components of your policy, regularly reviewing and updating it, and implementing risk management strategies, you can protect your home and assets effectively. Collaborating with reputable insurance professionals and staying informed about policy options and discounts further enhances your coverage, providing peace of mind against unexpected events.

References

- Homeowners Insurance Guide: A Beginner's Overview - Investopedia

- Searching for a Homeowners Insurance Policy? Tips to Get the Most Value - NAIC

- Tips for Homeowners' Insurance Coverage - Brooks, Todd & McNeil

- How much homeowners insurance do I need? | III

- 6 Things Your Homeowners Insurance Should Include - Unruh Insurance

- National Association of Insurance Commissioners (NAIC) - Homeowners Insurance Overview

- Bankrate - How Much Homeowners Insurance Coverage Do You Need?

- NerdWallet - Personal Property and Home Insurance Tips

- Home Insurance Coverage Considerations - Nationwide

- Tips to Make Sure Your Home Insurance Covers Your Needs - Independent Insurance Associates

- Tips for Lowering Your Homeowners Insurance - Liberty Mutual

- Dos and Don'ts When Insuring Your Home - UpHelp

Last updated January 24, 2025