Integrating Systematic Strategies in a Portfolio

A comprehensive guide to sizing and rebalancing multiple systematic strategies

Key Highlights

- Strategic Asset Allocation: Establish clear investment goals, risk tolerance, and target allocations across asset classes.

- Discipline in Rebalancing: Use systematic rules-based approaches such as calendar, threshold, or hybrid methods to maintain desired portfolio weights.

- Position Sizing & Risk Management: Implement methodologies such as Kelly Criterion, risk parity, and volatility-based adjustments to optimize exposure.

Understanding the Foundations of Portfolio Sizing

The Role of Investment Goals and Risk Tolerance

The first step in integrating systematic strategies in a portfolio is defining your investment objectives. Every investor has unique financial goals—whether it is capital growth, income generation, or a balanced approach—that determine the type of systematic strategies that should be incorporated. Equally important is your risk tolerance. This involves identifying how much deviation from your expected returns you can withstand without causing undue stress or forcing premature liquidation of positions during market downturns. Establishing a clear profile of your risk appetite and investment timeline shapes the strategic asset allocation that underpins your portfolio.

Establishing Target Asset Allocation

Once your investment goals and risk tolerance are clear, the next step is determining your target asset allocation across multiple asset classes such as stocks, bonds, real estate, and alternative investments. This allocation will serve as a roadmap to ensure that your portfolio is balanced and that each asset class contributes appropriately to your desired risk profile. The target allocation is based on risk management and long-term growth objectives. Different systematic strategies may focus on various market segments or factors, and recognizing the interplay between these strategies is crucial.

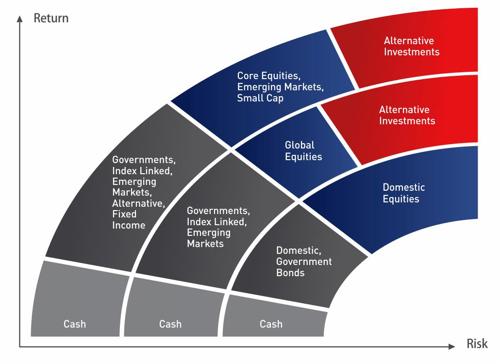

Diversification Across Asset Classes

Diversification is a core principle in portfolio construction. Allocating investments across uncorrelated asset classes minimizes the risk of significant losses, as the performance of one class typically does not mirror that of another. For instance, equities may exhibit high volatility compared to bonds, which usually have a more stable performance profile. By diversifying, you reduce the overall risk while creating an opportunity for smoother cumulative returns.

Sizing Systematic Strategies within a Portfolio

Framework for Position Sizing

Position sizing is fundamental to incorporating multiple systematic strategies into a portfolio. It involves determining how much capital to allocate to each strategy by considering the expected risk and return profiles, as well as how each strategy interacts with the overall portfolio risk. The following methodologies provide a structured approach to position sizing:

Kelly Criterion

The Kelly Criterion is a mathematical formula that helps determine the optimal bet size based on the probability of winning and losing. It is designed to maximize long-term portfolio growth while preventing the substantial losses that can occur with overly aggressive betting. By calculating a fraction of capital based on expected outcomes, the Kelly method maintains growth without exceeding a predetermined risk threshold.

Risk Parity

Risk parity involves allocating capital such that each asset or strategy contributes equally to the portfolio's overall risk. This approach ensures that lower volatility strategies do not disproportionately dominate larger, riskier allocations. By equalizing the risk contribution, you achieve a balanced portfolio where the collective risk exposure is distributed uniformly amongst the individual positions.

Volatility Position Sizing

Volatility-based position sizing adjusts the amount invested in each strategy depending on the current market volatility. During high-volatility periods, allocations to riskier strategies are reduced, while during stable market conditions, the allocation might be increased. This adaptive approach allows you to dynamically manage market fluctuations.

Maximum Drawdown Constraints

A prudent sizing strategy also considers maximum drawdowns—the peak-to-trough decline during market stress. This method sets a limit on the loss that any given strategy or the entire portfolio can endure, thereby controlling the downside risk.

In practice, combining these sizing methodologies can provide a robust framework for ensuring that individual systematic strategies are not over-leveraged and that the overall portfolio maintains a balanced exposure. This prevents excessive losses and preserves capital for long-term growth.

Systematic Rebalancing Strategies

Purpose of Rebalancing

Rebalancing is the systematic process of realigning the weightings of a portfolio's assets to maintain the original or desired asset allocation. Over time, market fluctuations cause asset classes to drift away from their target allocations, potentially increasing risk or deviating from the intended investment strategy. Systematic rebalancing ensures that the portfolio remains aligned with strategic investment objectives.

Methods of Rebalancing

There are several rebalancing methods available, each with its unique advantages and challenges. The most common approaches include calendar rebalancing, threshold-based rebalancing, and hybrid methods that combine elements of both.

Calendar-Based Rebalancing

This approach involves rebalancing the portfolio at predetermined intervals, such as quarterly or annually. The advantage of calendar rebalancing is its simplicity and minimal need for constant monitoring. However, it can lead to unnecessary trading if there has been little deviation from the target allocation or conversely, may miss significant deviations occurring between rebalancing periods.

Threshold-Based Rebalancing

Threshold-based rebalancing involves rebalancing only when the asset allocation drifts beyond a pre-set percentage. For instance, if the portfolio deviates by more than 5% from the target allocation in any asset class, a rebalance is triggered. This dynamic method is more responsive to market movements and helps avoid excessive trades when the portfolio remains relatively balanced.

Hybrid Rebalancing

A hybrid approach combines regular calendar rebalancing with threshold rules. This means that even if thresholds are not breached, a periodic review is conducted to ensure that the portfolio hasn’t strayed significantly from its prescribed allocation. This method optimizes the benefits of both approaches by balancing trade frequency with precision.

Practical Considerations in Implementing Rebalancing

Effective rebalancing in a portfolio involves several practical considerations. Transaction costs and tax implications should be minimized, which might involve using new contributions or withdrawals to adjust positions rather than selling existing holdings that have appreciated. Developing a disciplined, data-driven approach that removes emotion from the process is crucial for long-term success.

Transaction Costs and Tax Efficiency

Rebalancing can incur transaction fees and tax liabilities from selling and realizing capital gains. To mitigate these issues, investors often use techniques such as tax-loss harvesting, where losses are used to offset gains, and direct new contributions to underweighted areas of the portfolio. This helps maintain a balanced allocation without unnecessarily incurring extra costs.

Automation and Advanced Tools

Today, many investors leverage technological advances to automate rebalancing processes. Sophisticated algorithms monitor allocations in real time, trigger adjustments based on preset thresholds, and simulate the impact of different rebalancing scenarios. Automation not only removes emotional bias but also ensures a disciplined adherence to the strategy, which is particularly important when managing multiple strategies simultaneously.

Constructing a Multi-Strategy Portfolio

Combining Diverse Systematic Strategies

Integrating various systematic strategies into a single portfolio involves more than just allocating capital; it requires understanding how different strategies interact. Each systematic strategy has distinct market exposures and may perform differently under varying economic conditions. The goal is to combine strategies that are either uncorrelated or negatively correlated, thus reducing overall portfolio risk and enhancing returns over time.

Diversification Across Strategies

While diversification is often discussed in the context of asset classes, it is equally important to diversify within the realm of systematic strategies. For example, combining momentum-based strategies with value or contrarian approaches can create a robust diversified system. Because market conditions shift, having a mix of strategies can lead to smoother performance over multiple business cycles.

Utilizing Quantitative Models

Quantitative models provide objective measures to evaluate the risk and performance metrics of each strategy. These models can incorporate market sentiment indicators, macroeconomic data, and past performance metrics to predict future behavior under stress. By applying these tools, investors can determine appropriate capital allocation levels for each strategy and adjust them dynamically as market conditions evolve.

Risk Management and Continuous Monitoring

Risk management is at the core of successful portfolio construction. It involves continuous monitoring of both individual strategies and the portfolio as a whole. Keeping track of correlations between strategies, their individual volatilities, and maximum drawdown thresholds is critical. Regular performance evaluations help identify if any strategy deviates from expected behavior or if its risk contribution becomes disproportionate. Adjustments can then be made using rebalancing techniques.

Change in Market Environment

Global economic trends, interest rate fluctuations, geopolitical events, and technological advancements (such as AI-driven trading algorithms) can all affect systematic strategies differently. Therefore, a periodic review is necessary to ensure that each strategy continues to align with your overall investment goals. The integration of dynamic asset allocation allows portfolios to remain nimble and responsive to shifts in market conditions.

Rebalancing Techniques: A Comparative Overview

To better understand the different rebalancing strategies available, consider the following table which summarizes the main features of each method:

| Rebalancing Strategy | Key Features | Advantages | Considerations |

|---|---|---|---|

| Calendar-Based | Fixed intervals (e.g., quarterly, annually) | Simplicity, predictable schedule | May trade unnecessarily if allocation drifts little |

| Threshold-Based | Triggered by deviation percentage (e.g., 5% drift) | Responsive to market fluctuations | Requires frequent monitoring and may lead to higher transaction costs |

| Hybrid Approach | Combines calendar and threshold methods | Balances systematic scheduling with responsiveness | Complex setup and requires robust monitoring systems |

| Risk-Based | Adjusts allocations based on risk contributions | Maintains consistent overall portfolio risk | Relies on accurate risk estimation and continuous recalibration |

This table provides a comparative overview of popular rebalancing techniques, emphasizing that each method has unique benefits and challenges. The choice of strategy is influenced by an investor's overall portfolio objectives, risk tolerance, transaction cost considerations, and the desired level of automation.

Implementing a Disciplined System for Ongoing Management

Setting Up Clear Rebalancing Triggers

Establishing clear rebalancing triggers ensures that your portfolio remains in line with its target asset allocation. Triggers may be set on a calendar basis, when allocations drift past a set threshold, or through automated signals from quantitative models and algorithms. Whatever the trigger, the important aspect is consistency and discipline—determining in advance how, when, and by how much to adjust the allocations.

Integrating New Contributions and Withdrawals

One effective way to reduce the need for selling positions (and thus incurring tax liabilities) is to use new contributions or withdrawals to assist in rebalancing. Instead of liquidating high-performing assets to buy underweighted ones, redirecting fresh funds into these areas maintains the intended allocation while deferring taxable events. This approach not only minimizes transaction costs but also preserves the integrity of your long-term strategy.

Leveraging Advanced Technology

Modern portfolio management systems often come equipped with sophisticated algorithms that monitor real-time market data and provide systematic rebalancing recommendations. Automated portfolio rebalancing software can track deviations, calculate optimal trade sizes based on pre-determined sizing methodologies, and even execute trades within defined parameters. Utilizing such technology can significantly improve the precision and consistency of your portfolio adjustments.

Moreover, with the growing integration of artificial intelligence and advanced analytics, investors now have access to tools that simulate various rebalancing outcomes based on different market scenarios. This functionality not only increases the accuracy of rebalancing decisions but also aids in preparing for future market volatility.

Conclusion

Successfully sizing and rebalancing multiple systematic strategies into a portfolio demands a disciplined, structured, and analytical approach. It begins with clearly defined investment objectives and a precise understanding of your risk tolerance. Establishing a strategic asset allocation is foundational to guide the initial distribution of capital. A comprehensive approach must integrate reliable position sizing techniques—such as the Kelly Criterion, risk parity, and volatility-based adjustments—to optimize the allocation of capital across various strategies.

Rebalancing, as a systematic process, is critical in ensuring that your portfolio remains aligned with long-term goals despite market fluctuations. Whether using calendar-based, threshold-based, hybrid, or risk-based rebalancing methods, each requires careful planning to minimize transaction costs, reduce tax liabilities, and harness technology effectively. Integrating these methodologies with continuous monitoring and periodic reviews allows for dynamic adjustments in response to shifts in the global market environment or changes in individual performance metrics.

Ultimately, the key to success lies in creating a resilient portfolio that leverages the strengths of diverse systematic strategies while mitigating inherent risks. A disciplined and methodical approach helps in navigating market volatility, capitalizing on opportunities, and achieving sustainable long-term growth. By remaining focused on your core investment objectives and systematically reviewing your portfolio’s composition, you can maintain an optimal balance that is responsive to changing market dynamics and aligned with your financial goals.

References

- Model Portfolio Allocation - Vanguard

- Systematic Rebalancing Approaches - TraderHQ

- Rebalancing Strategies - Investopedia

- RAFI Fundamental Indices - RAFI

- Index Rebalance Trading Strategy - Quantified Strategies

Recommended Queries

Last updated February 22, 2025