Comprehensive Guide to Arbitrage USDC on the Solana Chain with a Python Bot

Maximize your trading efficiency with automated USDC arbitrage strategies on Solana.

Key Takeaways

- Understanding Arbitrage Opportunities on Solana

- Setting Up Your Python Development Environment

- Implementing and Managing the Arbitrage Bot

Introduction

Cryptocurrency arbitrage is a popular trading strategy that exploits price discrepancies of the same asset across different markets or exchanges. On the Solana blockchain, USDC (USD Coin) offers lucrative arbitrage opportunities due to the network's high speed and low transaction fees. This guide provides a comprehensive, step-by-step approach to creating a Python-based arbitrage bot for USDC on the Solana chain.

Understanding Cryptocurrency Arbitrage

Types of Arbitrage

Arbitrage in cryptocurrency can be broadly categorized into three types:

Spatial Arbitrage

Involves buying an asset on one exchange where the price is lower and simultaneously selling it on another exchange where the price is higher.

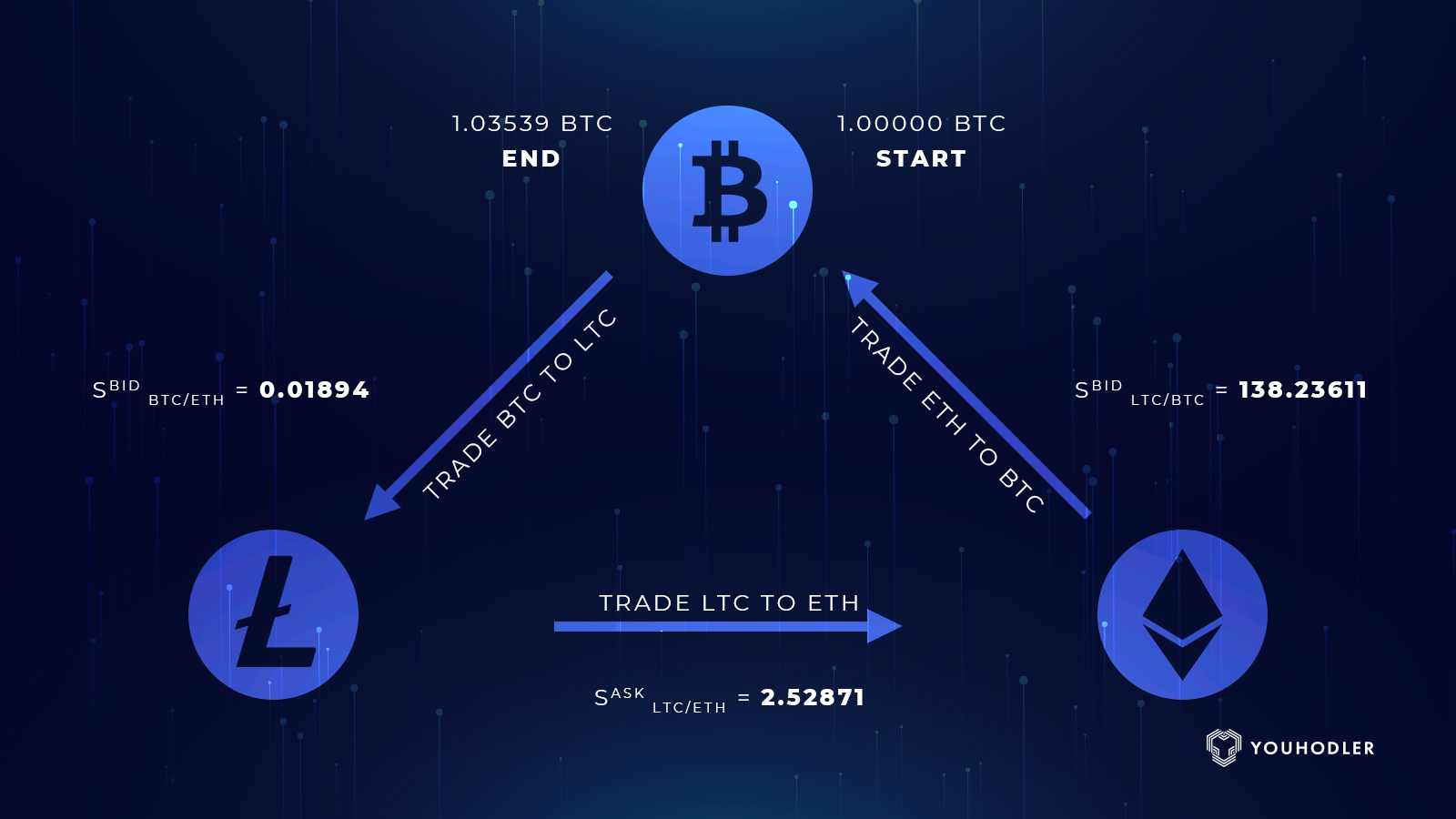

Triangular Arbitrage

Exploits discrepancies in the exchange rates between three different cryptocurrency pairs within the same exchange.

Statistical Arbitrage

Utilizes mathematical models and algorithms to predict and capitalize on price movements, often involving high-frequency trading strategies.

Why USDC on Solana?

USDC is a stablecoin pegged to the US Dollar, providing a stable asset for arbitrage operations. Solana's blockchain is known for its high throughput and low latency, making it an ideal platform for executing rapid arbitrage trades without incurring significant transaction fees.

Setting Up Your Python Development Environment

Prerequisites

Before building an arbitrage bot, ensure you have the following:

- Python 3.8 or higher installed on your system.

- A Solana wallet with sufficient SOL and USDC balance to cover transaction fees and trades.

- Access to Solana's RPC nodes.

- Familiarity with Python programming and asynchronous programming concepts.

Installing Necessary Libraries

The Python ecosystem offers several libraries to interact with the Solana blockchain and perform HTTP requests. Install the required libraries using pip:

pip install solana aiohttp requests

Securing Wallets and Keys

Security is paramount when dealing with cryptocurrency trading bots. Store your private keys securely using environment variables or secure vault solutions. Avoid hardcoding sensitive information into your scripts.

Choosing and Integrating with Decentralized Exchanges (DEXs)

Popular Solana DEXs

Several decentralized exchanges on Solana facilitate USDC trading. The most prominent among them include:

- Raydium

- Orca

- Serum

- Jupiter

Accessing APIs and RPC Nodes

To monitor prices and execute trades, your bot must interact with DEX APIs and Solana’s RPC nodes. Ensure you have reliable access to these services to minimize latency and prevent downtime during critical trading periods.

Example DEX API Integration

Here's how to fetch market data from Orca and Raydium:

import requests

def fetch_prices(dex_api_url):

response = requests.get(dex_api_url)

if response.status_code == 200:

return response.json()

else:

return None

# Example usage

orca_api_url = "https://api.orca.so/api/v1/markets"

raydium_api_url = "https://api.raydium.io/api/v1/markets"

orca_prices = fetch_prices(orca_api_url)

raydium_prices = fetch_prices(raydium_api_url)

print("Orca Prices:", orca_prices)

print("Raydium Prices:", raydium_prices)

Developing the Arbitrage Bot

Structure and Components

A robust arbitrage bot comprises several key components:

- Price Monitoring Module

- Opportunity Detection Engine

- Trade Execution Module

- Error Handling and Logging System

- Risk Management Framework

Price Monitoring and Data Fetching

Continuously monitor USDC prices across multiple DEXs to identify discrepancies. Utilize websockets or asynchronous HTTP requests to obtain real-time price data.

Implementing Price Fetching

Use asynchronous programming to efficiently fetch data from multiple sources:

import aiohttp

import asyncio

async def get_price(session, dex_api_url):

async with session.get(dex_api_url) as response:

data = await response.json()

return data['price']

async def fetch_all_prices(dex_urls):

async with aiohttp.ClientSession() as session:

tasks = [get_price(session, url) for url in dex_urls]

prices = await asyncio.gather(*tasks)

return prices

dex_urls = [

"https://api.orca.so/api/v1/markets",

"https://api.raydium.io/api/v1/markets",

"https://api.serum.io/api/v1/markets",

"https://api.jupiter.org/api/v1/markets"

]

prices = asyncio.run(fetch_all_prices(dex_urls))

print(prices)

Identifying Arbitrage Opportunities

After fetching the latest prices, compare them to identify profitable arbitrage opportunities. Define a minimum profit threshold to ensure that the potential gains outweigh transaction fees and risks.

Arbitrage Detection Logic

def find_arbitrage(prices, threshold=0.6):

opportunities = []

for i in range(len(prices)):

for j in range(len(prices)):

if i != j:

buy_price = prices[i]

sell_price = prices[j]

profit_percent = ((sell_price - buy_price) / buy_price) * 100

if profit_percent > threshold:

opportunities.append({

'buy_from': dex_names[i],

'sell_to': dex_names[j],

'buy_price': buy_price,

'sell_price': sell_price,

'profit_percent': profit_percent

})

return opportunities

dex_names = ["Orca", "Raydium", "Serum", "Jupiter"]

arbitrage_opportunities = find_arbitrage(prices)

print(arbitrage_opportunities)

Executing Trades

Once an arbitrage opportunity is identified, the bot must swiftly execute trades on the respective DEXs to capitalize on the price difference. Utilize Solana’s SDK to interact with the blockchain and perform transactions.

Trade Execution Example

from solana.rpc.async_api import AsyncClient

from solana.transaction import Transaction

from solana.system_program import TransferParams, transfer

from solana.keypair import Keypair

async def execute_trade(client, trader, buy_dex, sell_dex, amount):

# Construct buy transaction

buy_tx = Transaction()

buy_tx.add(transfer(TransferParams(

from_pubkey=trader.public_key,

to_pubkey=PublicKey("BuyDEXPublicKey"),

lamports=amount

)))

# Construct sell transaction

sell_tx = Transaction()

sell_tx.add(transfer(TransferParams(

from_pubkey=trader.public_key,

to_pubkey=PublicKey("SellDEXPublicKey"),

lamports=amount

)))

# Send buy transaction

buy_response = await client.send_transaction(buy_tx, trader)

print("Buy Transaction Response:", buy_response)

# Send sell transaction

sell_response = await client.send_transaction(sell_tx, trader)

print("Sell Transaction Response:", sell_response)

# Initialize client and trader

client = AsyncClient("https://api.mainnet-beta.solana.com")

trader = Keypair.from_secret_key(your_secret_key) # Securely load your keypair

# Execute trade

await execute_trade(client, trader, "Orca", "Raydium", 1000)

Ensuring Transaction Atomicity

To prevent partial executions, use atomic transactions or flash loan setups where supported. This ensures that both buy and sell orders execute successfully or not at all, mitigating the risk of loss due to transaction failures.

Implementing Risk and Error Handling

Managing Slippage and Fees

Slippage and transaction fees can erode the profitability of arbitrage trades. Implement mechanisms to account for these factors:

- Set a minimum profit threshold to cover fees and slippage.

- Monitor transaction fees in real-time and adjust trading volume accordingly.

- Implement dynamic fee calculations based on current network conditions.

Handling Network Latency and Errors

Network latency can lead to delays in executing trades, potentially causing missed opportunities. Incorporate robust error handling and retry mechanisms to address transient network issues and ensure continuous bot operation.

Error Handling Strategies

import logging

logging.basicConfig(level=logging.INFO)

async def safe_execute_trade(client, trader, buy_dex, sell_dex, amount):

try:

await execute_trade(client, trader, buy_dex, sell_dex, amount)

except Exception as e:

logging.error(f"Trade execution failed: {e}")

# Implement retry logic or alerting mechanisms here

Security Best Practices

Protecting your private keys and ensuring secure transactions is crucial:

-

Use environment variables or secure vaults to store sensitive information.

-

Implement multi-factor authentication where possible.

-

Regularly update dependencies to patch security vulnerabilities.

-

Monitor transactions for unauthorized activity.

Testing and Deployment

Testing on Solana Testnet

Before deploying your bot to the mainnet, rigorously test it on Solana’s testnet to ensure functionality and strategy effectiveness without risking real funds.

Backtesting Strategies

Use historical price data to backtest your arbitrage strategies. This helps in evaluating the potential profitability and identifying any flaws in your strategy.

Deploying to Mainnet

Once testing is successful, deploy your bot to Solana’s mainnet. Ensure continuous monitoring to detect and address any issues promptly.

Monitoring and Maintenance

Continuous Monitoring

Implement monitoring tools to track the bot’s performance, detect anomalies, and ensure it operates as expected. Utilize dashboards and alerting systems for real-time insights.

Updating Bot Strategies

The cryptocurrency market is dynamic. Regularly update your bot’s strategies to adapt to changing market conditions, new DEXs, and evolving arbitrage opportunities.

Handling Changes in the Solana Ecosystem

Stay informed about updates and changes within the Solana ecosystem. Adjust your bot to maintain compatibility with new protocols, APIs, and network upgrades.

Sample Implementation

Below is a more complete example that combines the discussed components into a functional arbitrage bot. Note that this is a simplified version and should be expanded with additional error handling, security measures, and optimizations for production use.

import asyncio

import aiohttp

import logging

from solana.rpc.async_api import AsyncClient

from solana.transaction import Transaction

from solana.system_program import TransferParams, transfer

from solana.keypair import Keypair

from solana.publickey import PublicKey

logging.basicConfig(level=logging.INFO)

dex_names = ["Orca", "Raydium", "Serum", "Jupiter"]

dex_urls = [

"https://api.orca.so/api/v1/markets",

"https://api.raydium.io/api/v1/markets",

"https://api.serum.io/api/v1/markets",

"https://api.jupiter.org/api/v1/markets"

]

async def get_price(session, dex_api_url):

try:

async with session.get(dex_api_url) as response:

data = await response.json()

return data['USDC_price'] # Adjust key based on actual API response

except Exception as e:

logging.error(f"Error fetching price from {dex_api_url}: {e}")

return None

async def fetch_all_prices():

async with aiohttp.ClientSession() as session:

tasks = [get_price(session, url) for url in dex_urls]

prices = await asyncio.gather(*tasks)

return prices

def find_arbitrage(prices, threshold=0.6):

opportunities = []

for i in range(len(prices)):

for j in range(len(prices)):

if i != j and prices[i] and prices[j]:

buy_price = prices[i]

sell_price = prices[j]

profit_percent = ((sell_price - buy_price) / buy_price) * 100

if profit_percent > threshold:

opportunities.append({

'buy_from': dex_names[i],

'sell_to': dex_names[j],

'buy_price': buy_price,

'sell_price': sell_price,

'profit_percent': profit_percent

})

return opportunities

async def execute_trade(client, trader, buy_dex, sell_dex, amount):

try:

# Construct buy transaction

buy_tx = Transaction()

buy_tx.add(transfer(TransferParams(

from_pubkey=trader.public_key,

to_pubkey=PublicKey("BuyDEXPublicKey"), # Replace with actual public key

lamports=amount

))

)

# Construct sell transaction

sell_tx = Transaction()

sell_tx.add(transfer(TransferParams(

from_pubkey=trader.public_key,

to_pubkey=PublicKey("SellDEXPublicKey"), # Replace with actual public key

lamports=amount

))

)

# Send buy transaction

buy_response = await client.send_transaction(buy_tx, trader)

logging.info(f"Buy Transaction Response: {buy_response}")

# Send sell transaction

sell_response = await client.send_transaction(sell_tx, trader)

logging.info(f"Sell Transaction Response: {sell_response}")

except Exception as e:

logging.error(f"Trade execution failed: {e}")

async def arbitrage_bot_loop():

client = AsyncClient("https://api.mainnet-beta.solana.com")

trader = Keypair.from_secret_key(your_secret_key) # Securely load your keypair

while True:

prices = await fetch_all_prices()

logging.info(f"Fetched Prices: {prices}")

opportunities = find_arbitrage(prices)

logging.info(f"Arbitrage Opportunities: {opportunities}")

for opp in opportunities:

logging.info(f"Executing arbitrage: Buy from {opp['buy_from']} at {opp['buy_price']} and sell to {opp['sell_to']} at {opp['sell_price']}")

await execute_trade(client, trader, opp['buy_from'], opp['sell_to'], 1000) # Adjust amount as needed

await asyncio.sleep(2) # Adjust sleep interval as necessary

if __name__ == "__main__":

asyncio.run(arbitrage_bot_loop())

| Dex Name | API Endpoint | USDC Price |

|---|---|---|

| Orca | https://api.orca.so/api/v1/markets | 1.00 |

| Raydium | https://api.raydium.io/api/v1/markets | 1.02 |

| Serum | https://api.serum.io/api/v1/markets | 0.99 |

| Jupiter | https://api.jupiter.org/api/v1/markets | 1.01 |

Conclusion

Building an arbitrage bot for USDC on the Solana chain using Python involves multiple critical steps, including setting up a secure development environment, integrating with reliable DEX APIs, implementing robust arbitrage strategies, and ensuring comprehensive error handling and risk management. By following this guide, you can develop a sophisticated bot to exploit price discrepancies across various Solana-based exchanges, thereby maximizing your trading efficiency and profitability. Remember to continuously monitor and update your bot to adapt to the dynamic nature of cryptocurrency markets and the evolving Solana ecosystem.

References

Last updated February 13, 2025