Unlocking the Enduring Value of Whole Life Insurance Policies

A Comprehensive Guide to Lifelong Coverage and Financial Growth

Key Insights into Whole Life Insurance

- Permanent Protection: Whole life insurance offers coverage for your entire lifetime, ensuring a death benefit is paid to your beneficiaries regardless of when you pass away, as long as premiums are maintained.

- Guaranteed Cash Value Growth: A significant feature of whole life policies is their cash value component, which grows at a guaranteed rate on a tax-deferred basis, providing a living benefit that can be accessed during your lifetime.

- Fixed Premiums and Death Benefits: Unlike other insurance types, whole life policies are characterized by premiums that remain level throughout the policy's life and a death benefit that is fixed, offering predictability and stability in financial planning.

Whole life insurance stands as a cornerstone in the realm of permanent life insurance, designed to provide coverage that spans your entire lifetime. It's a comprehensive financial tool that not only offers a guaranteed death benefit to your beneficiaries upon your passing but also builds a cash value component that can be accessed while you are alive. This unique combination of lifelong protection and a growing savings element distinguishes whole life from other forms of life insurance, such as term life, which only covers a specific period.

The Core Mechanics of Whole Life Insurance

At its essence, a whole life insurance policy is a contract between the insured and the insurer. As long as the required premiums are paid, the insurer guarantees to pay a death benefit to the policy's beneficiaries when the insured dies. This lifelong guarantee is a primary appeal, providing enduring peace of mind for policyholders who wish to ensure their loved ones are financially protected long into the future.

Key Components of a Whole Life Policy

Every whole life insurance policy is built upon three fundamental elements:

Premiums: Consistent and Predictable Payments

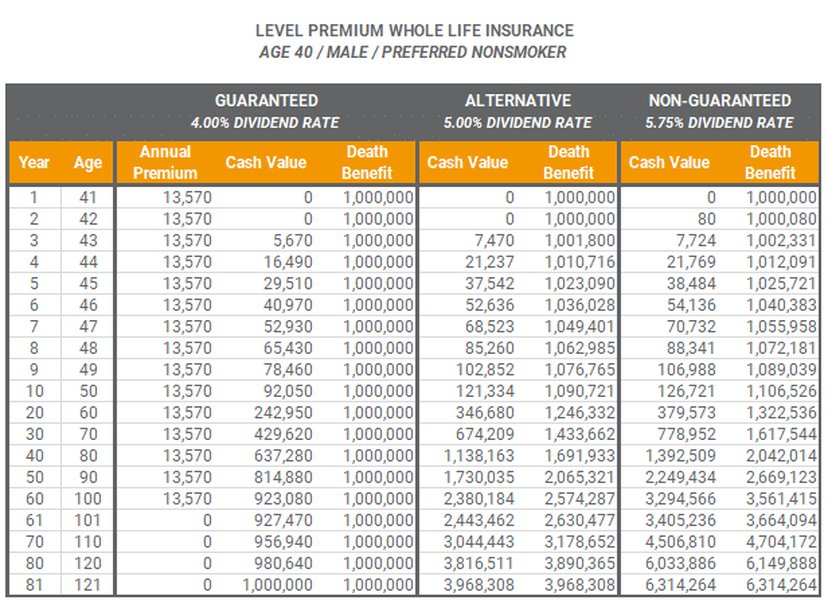

Whole life insurance is characterized by level premiums, meaning the payments remain fixed and consistent for the entire duration of the policy. These premiums are based on the age of issue and generally do not increase with age. A portion of each premium payment goes towards covering the "cost of insurance" (the death benefit), while the other portion contributes to the policy's cash value. This predictability in cost allows for easier long-term financial planning compared to policies where premiums may increase over time.

This chart illustrates how whole life insurance policies maintain level premiums throughout their duration, providing consistent costs for policyholders.

Death Benefit: Guaranteed Payout for Beneficiaries

The death benefit is the core purpose of any life insurance policy. In whole life insurance, this benefit is a fixed sum guaranteed to be paid to your designated beneficiaries upon your death. This guarantee holds true no matter when the insured passes away, providing a crucial financial safety net for loved ones to replace lost income, cover final expenses, or achieve other financial goals. Unlike some other permanent policies, the death benefit in whole life typically remains stable, offering certainty to your estate planning.

Cash Value: A Living Benefit with Guaranteed Growth

Perhaps one of the most distinctive features of whole life insurance is its cash value component. This is a savings element that accrues over time, growing at a guaranteed rate on a tax-deferred basis. As you pay premiums, a portion of that money is allocated to this cash value. This accumulated cash value offers several "living benefits" that policyholders can utilize during their lifetime:

- Policy Loans: You can borrow money against your policy's cash value. These loans are tax-free as long as the policy remains in force, and the interest rates are often competitive, sometimes even less than the dividends earned by participating policies.

- Withdrawals: While less common as they reduce the death benefit and cash surrender value, you can also withdraw funds from the cash value.

- Premium Payments: In some cases, the accumulated cash value can be used to pay future premiums, offering flexibility, especially in retirement.

- Surrender for Cash: You can surrender the policy for its cash value, although this would terminate the coverage.

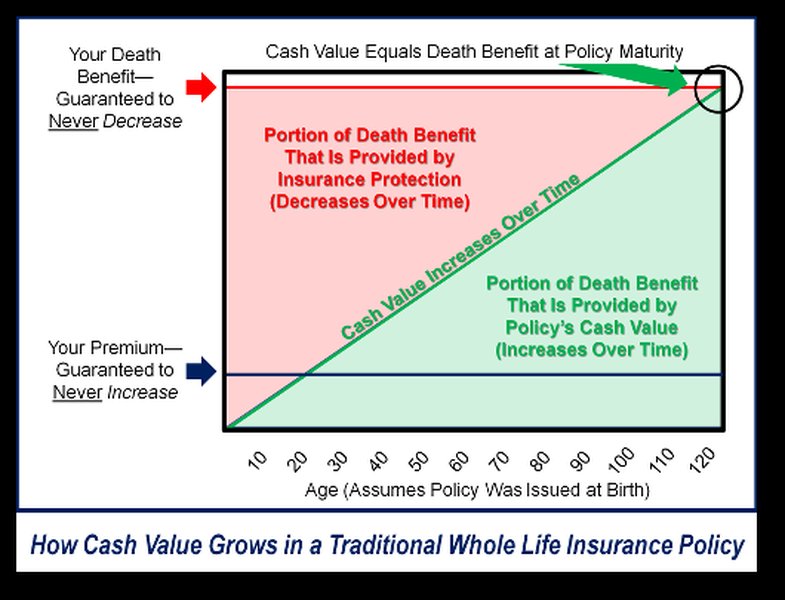

This graph illustrates the gradual accumulation of cash value within a whole life policy alongside the consistent death benefit.

Types of Whole Life Insurance Policies

While the fundamental principles remain consistent, whole life insurance can come with slight variations tailored to different needs:

Standard Whole Life

This is the most common form, where premiums are paid throughout the insured's lifetime until death or maturity (often age 100 or 121). It offers the greatest simplicity and predictability.

Limited Payment Whole Life

With this type, premiums are paid only for a specified period, such as 10 years, 20 years, or until a certain age (e.g., age 65). After this period, the policy is considered "paid up," meaning no further premiums are required, but the coverage and cash value growth continue for life.

A visual representation of a limited-pay whole life policy, highlighting the finite period of premium payments.

Modified Whole Life

This policy offers lower premiums during an initial period (e.g., the first 3-5 years) and then higher premiums for the remainder of the policy's life. The death benefit remains unchanged. This can be beneficial for individuals who anticipate higher income in the future.

Understanding the Value Proposition

Whole life insurance is often debated in terms of its "investment" potential compared to other financial vehicles. It's crucial to understand that while it has an investment component through its cash value, its primary function is long-term insurance coverage and financial security. The growth of the cash value is guaranteed, providing a safe and predictable asset, unlike market-based investments.

Whole Life Insurance vs. Term Life Insurance

A frequent comparison is made between whole life and term life insurance. Here’s a summary of their key differences:

| Feature | Whole Life Insurance | Term Life Insurance |

|---|---|---|

| Coverage Duration | Lifelong (permanent) | Specific period (e.g., 10, 20, 30 years) |

| Premiums | Fixed and level | Fixed for the term, can increase upon renewal |

| Cash Value | Builds cash value over time | No cash value component |

| Investment Component | Yes, guaranteed growth, tax-deferred | No |

| Flexibility | Less payment flexibility than universal life; cash value loans/withdrawals | Can be converted to permanent in some cases |

| Cost | Generally more expensive | Generally more affordable |

| Purpose | Lifelong protection, wealth building, estate planning | Temporary income replacement, specific financial needs |

The choice between whole life and term life often hinges on individual financial goals, budget, and the desired duration of coverage. Whole life suits those seeking lifelong protection and a guaranteed savings component, while term life is often preferred for affordable coverage over a specific period, such as during prime earning years or while raising a family.

The "Why" Behind Whole Life: A Deeper Look

To further contextualize the benefits and considerations of whole life insurance, let's explore its various facets through a radar chart. This chart will visually represent how whole life policies perform across several key dimensions, offering a multi-dimensional perspective.

This radar chart illustrates the key characteristics where whole life insurance typically excels compared to a general investment vehicle. Whole life policies stand out strongly in areas like Lifelong Coverage, Premium Stability, and Guaranteed Cash Value Growth, offering predictability and security. While a general investment vehicle might offer higher potential returns (represented here loosely by 'Liquidity Access' for quick cash), it typically lacks the guaranteed aspects of premiums and coverage that whole life provides. The chart emphasizes whole life's role as a foundational financial instrument for long-term security and wealth preservation, often serving as a reliable complement to more volatile market-based investments.

Accessing Your Whole Life Policy's Value

One of the appealing aspects of whole life insurance is the ability to access the cash value during your lifetime. This liquidity can be a valuable financial resource for various needs, from funding a child's education to supplementing retirement income or addressing unexpected emergencies.

How to Tap into Your Cash Value

There are generally a few ways to access the cash value built within a whole life policy:

- Policy Loans: This is the most common method. You can borrow against your cash value, and the loan is repaid with interest. The policy remains in force, and the death benefit is only reduced if the loan is not repaid by the time of your death.

- Withdrawals: You can withdraw a portion of your cash value. However, withdrawals reduce both the cash value and the death benefit of the policy.

- Surrendering the Policy: You can surrender the policy for its cash surrender value. This means you cancel the policy, and the insurer pays you the accumulated cash value, minus any surrender charges. This, of course, terminates the insurance coverage.

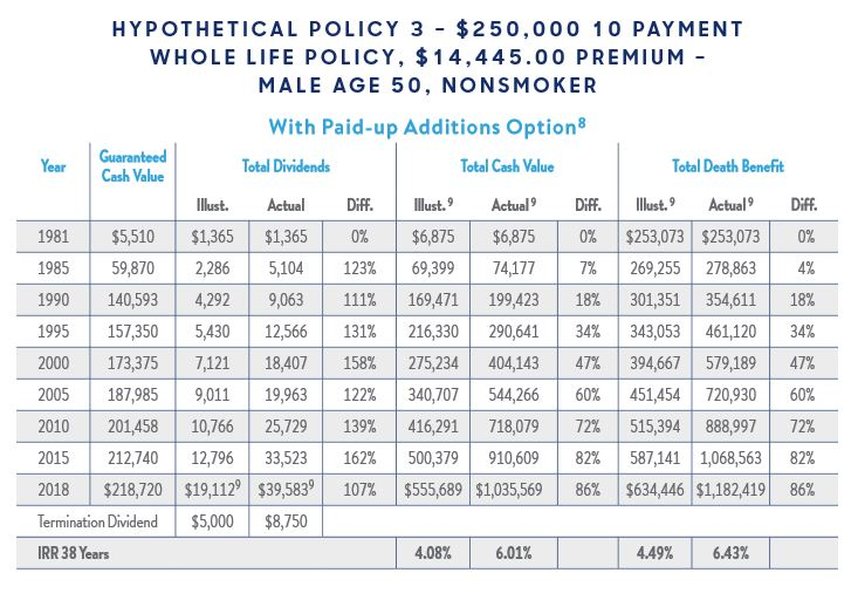

- Using Dividends: If you have a participating whole life policy (often from mutual insurance companies), you may receive annual dividends. These can be taken as cash, used to reduce premiums, or reinvested to purchase paid-up additions, which increase both the cash value and death benefit.

Considerations Before Choosing Whole Life

While whole life insurance offers significant benefits, it's important to consider all aspects to determine if it aligns with your financial strategy.

Cost Implications

Whole life insurance premiums are generally more expensive than term life insurance for the same death benefit amount, especially in the initial years. This higher cost reflects the lifelong coverage, guaranteed cash value growth, and other features. For example, a healthy non-smoking 40-year-old man might pay around $7,440 annually for a $500,000 whole life policy, whereas a 20-year term policy for the same amount might cost only $334 per year.

Financial Goals Alignment

Whole life insurance is best suited for individuals who prioritize lifelong protection, wealth preservation, and tax-advantaged savings with guaranteed growth. It can be a valuable tool for estate planning, ensuring liquidity for heirs, or supplementing retirement income. However, if your primary need is temporary coverage for a specific period (e.g., during mortgage repayment or until children are grown), a term life policy might be more appropriate and cost-effective.

Here is a video that provides an excellent overview of how whole life insurance policies work, covering many of the concepts discussed:

This video, "Whole Life Insurance For Dummies," offers a concise and easy-to-understand explanation of whole life insurance, making complex concepts accessible to a broad audience.

Frequently Asked Questions

Conclusion

Whole life insurance offers a distinctive blend of guaranteed lifelong protection and a steadily growing cash value component. Its fixed premiums and death benefits provide financial predictability, making it a powerful tool for long-term financial planning, wealth preservation, and estate planning. While generally more expensive than term life insurance, its living benefits, such as the ability to borrow against the cash value, and its tax advantages can make it a worthwhile consideration for individuals seeking comprehensive and enduring financial security for themselves and their loved ones.

Recommended Further Exploration

- Explore the various ways to leverage the cash value in a whole life insurance policy.

- Understand the nuances between whole life and other permanent life insurance options like universal life.

- Delve deeper into the tax efficiencies associated with whole life insurance policies.

- Learn how to assess your personal financial needs to select the most suitable life insurance coverage.

References

Last updated May 21, 2025